Answered step by step

Verified Expert Solution

Question

1 Approved Answer

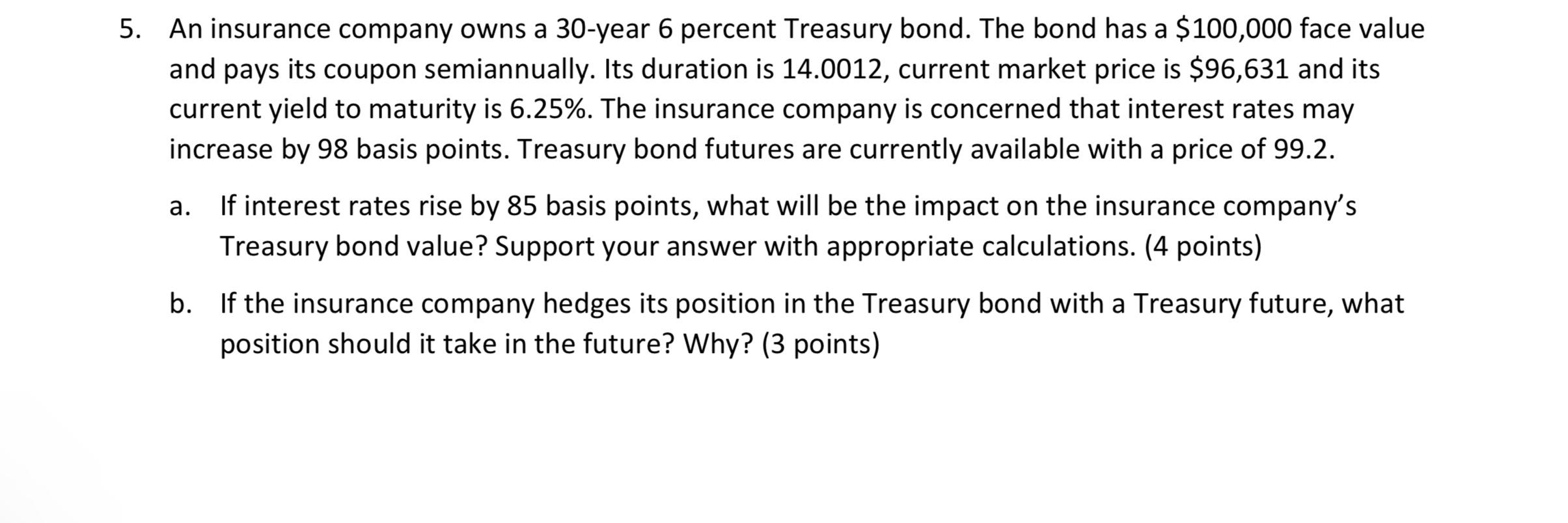

5. An insurance company owns a 30 -year 6 percent Treasury bond. The bond has a $100,000 face value and pays its coupon semiannually. Its

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quantitative Analysis for Management

Authors: Barry Render, Ralph M. Stair, Michael E. Hanna, Trevor S. Ha

12th edition

133507335, 978-0133507331