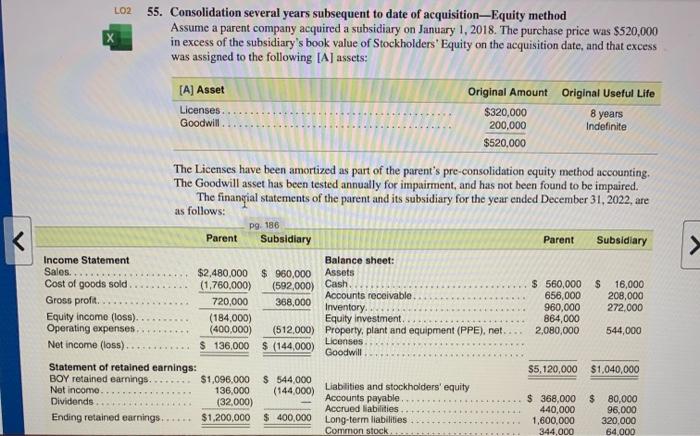

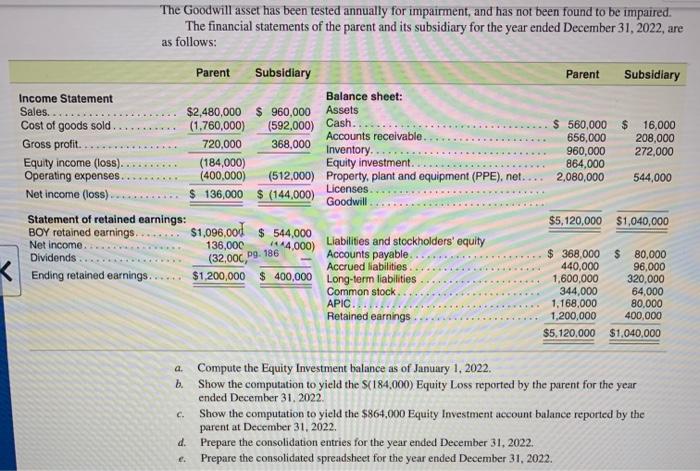

5. Consolidation several years subsequent to date of acquisition-Equity method Assume a parent company acquired a subsidiary on January 1, 2018. The purchase price was $520,000 in excess of the subsidiary's book value of Stockholders' Equity on the aequisition date, and that excess was assigned to the following [A] assets: The Licenses have been amortized as part of the parent's pre-consolidation equity method accounting. The Goodwill asset has been tested annually for impairment, and has not been found to be impaired. The finanyial statements of the parent and its subsidiary for the year ended December 31,2022 , are as follows: The Goodwill asset has been tested annually for impairment, and has not been found to be impaired. The financial statements of the parent and its subsidiary for the year ended December 31, 2022, are as follows: a. Compute the Equity Investment balance as of January 1, 2022 . b. Show the computation to yield the $(184,000) Equity Loss reported by the purent for the year ended December 31, 2022. c. Show the computation to yield the $864,000 Equity Investment account balance reported by the parent at December 31, 2022. d. Prepare the consolidation entries for the year ended December 31, 2022. e. Prepare the consolidated spreadsheet for the year ended December 31, 2022 . 5. Consolidation several years subsequent to date of acquisition-Equity method Assume a parent company acquired a subsidiary on January 1, 2018. The purchase price was $520,000 in excess of the subsidiary's book value of Stockholders' Equity on the aequisition date, and that excess was assigned to the following [A] assets: The Licenses have been amortized as part of the parent's pre-consolidation equity method accounting. The Goodwill asset has been tested annually for impairment, and has not been found to be impaired. The finanyial statements of the parent and its subsidiary for the year ended December 31,2022 , are as follows: The Goodwill asset has been tested annually for impairment, and has not been found to be impaired. The financial statements of the parent and its subsidiary for the year ended December 31, 2022, are as follows: a. Compute the Equity Investment balance as of January 1, 2022 . b. Show the computation to yield the $(184,000) Equity Loss reported by the purent for the year ended December 31, 2022. c. Show the computation to yield the $864,000 Equity Investment account balance reported by the parent at December 31, 2022. d. Prepare the consolidation entries for the year ended December 31, 2022. e. Prepare the consolidated spreadsheet for the year ended December 31, 2022