Answered step by step

Verified Expert Solution

Question

1 Approved Answer

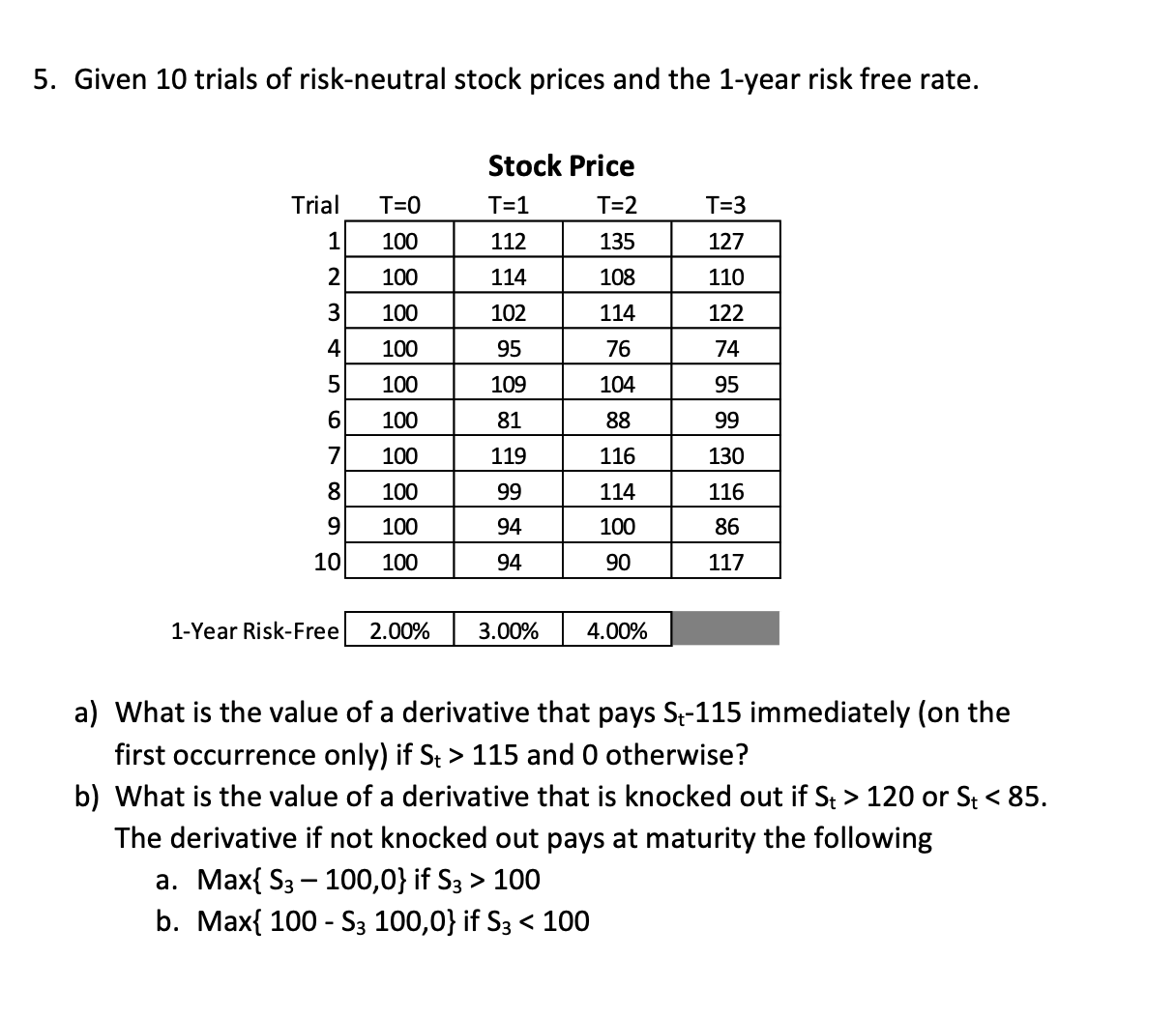

5. Given 10 trials of risk-neutral stock prices and the 1-year risk free rate. begin{tabular}{l|l|l|l|} cline { 2 - 3 } 1 1-Year Risk-Free 2.00%

5. Given 10 trials of risk-neutral stock prices and the 1-year risk free rate. \begin{tabular}{l|l|l|l|} \cline { 2 - 3 } 1 1-Year Risk-Free 2.00% & 3.00% & 4.00% \\ \hline \end{tabular} a) What is the value of a derivative that pays St115 immediately (on the first occurrence only) if St>115 and 0 otherwise? b) What is the value of a derivative that is knocked out if St>120 or St100 b. Max{100S3100,0} if S3

5. Given 10 trials of risk-neutral stock prices and the 1-year risk free rate. \begin{tabular}{l|l|l|l|} \cline { 2 - 3 } 1 1-Year Risk-Free 2.00% & 3.00% & 4.00% \\ \hline \end{tabular} a) What is the value of a derivative that pays St115 immediately (on the first occurrence only) if St>115 and 0 otherwise? b) What is the value of a derivative that is knocked out if St>120 or St100 b. Max{100S3100,0} if S3 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Building Financial Models

Authors: John Tjia

2nd Edition

0071608893, 978-0071608893