Answered step by step

Verified Expert Solution

Question

1 Approved Answer

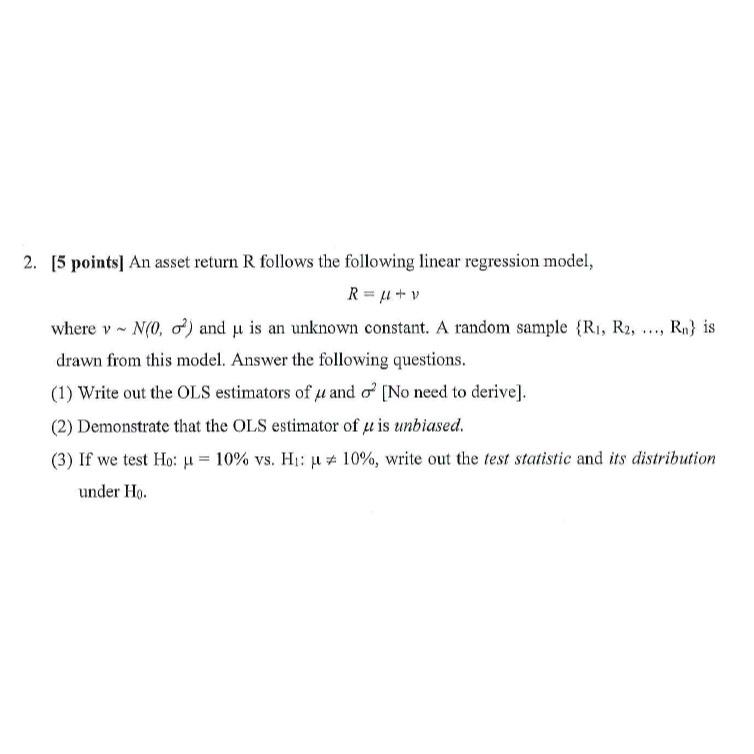

[ 5 points ] An asset return R follows the following linear regression model, R = + v where v N ( 0 , 2

points An asset return follows the following linear regression model,

where and is an unknown constant. A random sample dots, is drawn from this model. Answer the following questions.

Write out the OLS estimators of and No need to derive

Demonstrate that the OLS estimator of is unbiased.

If we test : vs: write out the test statistic and its distribution under

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Theory and Corporate Policy

Authors: Thomas E. Copeland, J. Fred Weston, Kuldeep Shastri

4th edition

321127218, 978-0321179548, 321179544, 978-0321127211