Answered step by step

Verified Expert Solution

Question

1 Approved Answer

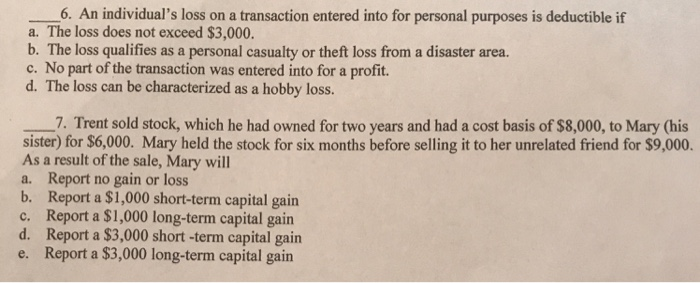

6. An individual's loss on a transaction entered into for personal purposes is deductible if a. The loss does not exceed $3,000. b. The loss

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Medical Audit In Primary Health Care

Authors: Martin Lawrence, Theo Schofield

1st Edition

0192622676, 978-0192622679