Answered step by step

Verified Expert Solution

Question

1 Approved Answer

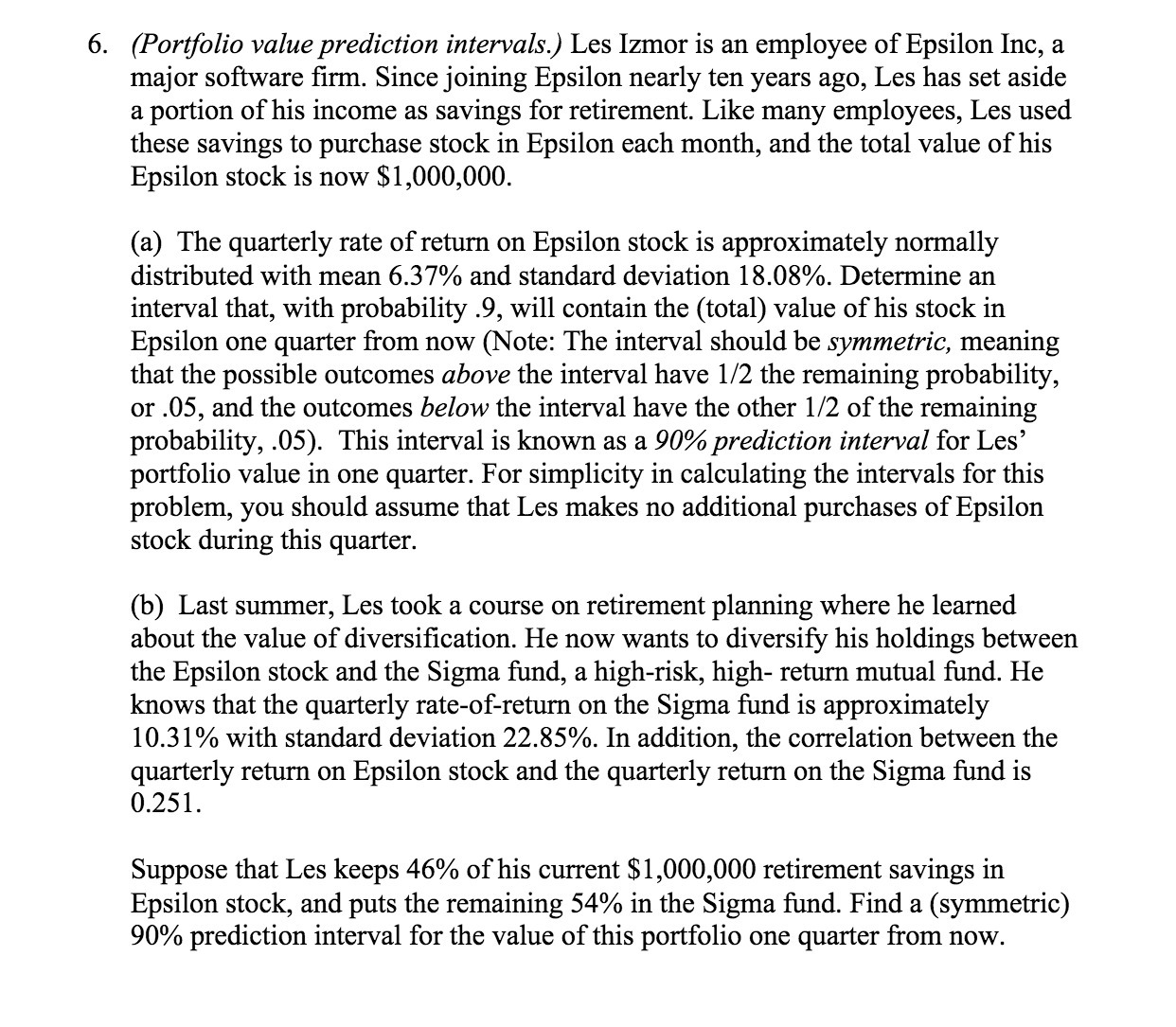

6. (Pory'olio value prediction intervals.) Les Izmor is an employee of Epsilon Inc, a major software rm. Since joining Epsilon nearly ten years ago, Les

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Business Statistics for Contemporary Decision Making

Authors: Ken Black

6th Edition

978-0470409015, 9780470559062, 470409010, 470559063, 978-0470910184