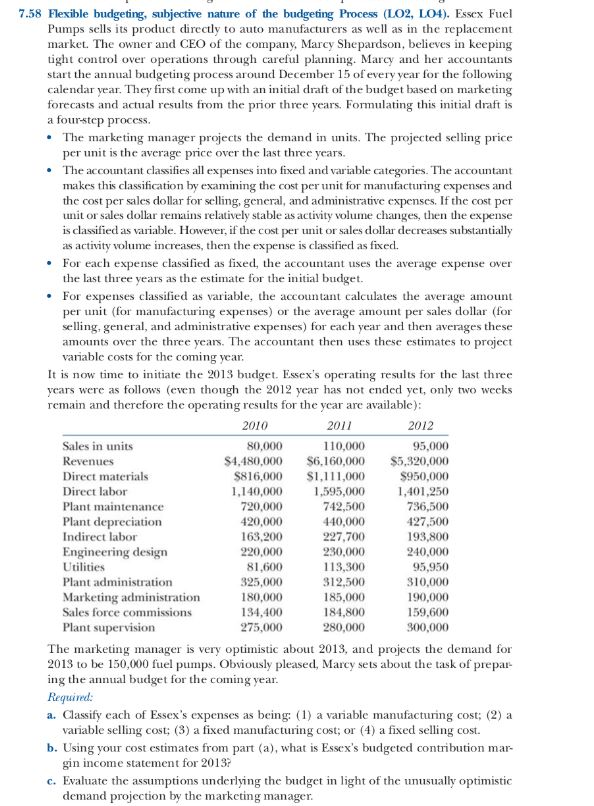

7.58 Flexible budgeting, subjective nature of the budgeting Process (LO2, LO4). Essex Fuel Pumps sells its product directly to auto manufacturers as well as in the replacement market. The owner and CEO of the company, Marcy Shepardson, believes in keeping tight control over operations through careful planning. Marcy and her accountants start the annual budgeting process around December 15 of every year for the following calendar year. They first come up with an initial draft of the budget based on marketing forecasts and actual results from the prior three years. Formulating this initial draft is a four-step process. The marketing manager projects the demand in units. The projected selling price per unit is the average price over the last three years. The accountant classifies all expenses into fixed and variable categories. The accountant makes this classification by examining the cost per unit for manufacturing expenses and the cost per siles dollar for selling general, and administrative expenses. If the cost per unitor sales dollar remains relatively stable as activity volume changes, then the expense is classified as variable. However, if the cost per unit or sales dollar decreases substantially as activity volume increases, then the expense is classified as fixed. For each expense classified as fixed, the accountant uses the average expense over the last three years as the estimate for the initial budget. For expenses classified as variable, the accountant calculates the average amount per unit (for manufacturing expenses) or the average amount per sales dollar (for selling, general, and administrative expenses) for each year and then averages these amounts over the three years. The accountant then uses these estimates to project variable costs for the coming year. It is now time to initiate the 2013 budget. Essex's operating results for the last three years were as follows (even though the 2012 year has not ended yet, only two weeks remain and therefore the operating results for the year are available): 2010 2011 2012 Sales in units 80,000 110.000 95,000 Revenues $4,480,000 $6,160,000 $5,320,000 Direct materials $816,000 $1,111,000 $950,000 Direct labor 1.140,000 1.595,000 1,401,250 Plant maintenance 720,000 742,500 736,500 Plant depreciation 420,000 440,000 427,500 Indirect labor 163,200 227,700 193,800 Engineering design 220,000 230,000 240,000 Utilities 81,600 113,300 95,950 Plant administration 325,000 312,500 310,000 Marketing administration 180,000 185,000 190,000 Sales force commissions 134,400 184,800 159,600 Plant supervision 275,000 280,000 300,000 The marketing manager is very optimistic about 2013, and projects the demand for 2013 to be 150,000 fuel pumps. Obviously pleased, Marcy sets about the task of prepar- ing the annual budget for the coming year. Required: a. Classify each of Essex's expenses as being: (1) a variable manufacturing cost; (2) a variable selling cost; (3) a fixed manufacturing cost; or (4) a fixed selling cost b. Using your cost estimates from part (a), what is Essex's budgeted contribution mar- gin income statement for 2013? c. Evaluate the assumptions underlying the budget in light of the unusually optimistic demand projection by the marketing manager. 7.58 Flexible budgeting, subjective nature of the budgeting Process (LO2, LO4). Essex Fuel Pumps sells its product directly to auto manufacturers as well as in the replacement market. The owner and CEO of the company, Marcy Shepardson, believes in keeping tight control over operations through careful planning. Marcy and her accountants start the annual budgeting process around December 15 of every year for the following calendar year. They first come up with an initial draft of the budget based on marketing forecasts and actual results from the prior three years. Formulating this initial draft is a four-step process. The marketing manager projects the demand in units. The projected selling price per unit is the average price over the last three years. The accountant classifies all expenses into fixed and variable categories. The accountant makes this classification by examining the cost per unit for manufacturing expenses and the cost per siles dollar for selling general, and administrative expenses. If the cost per unitor sales dollar remains relatively stable as activity volume changes, then the expense is classified as variable. However, if the cost per unit or sales dollar decreases substantially as activity volume increases, then the expense is classified as fixed. For each expense classified as fixed, the accountant uses the average expense over the last three years as the estimate for the initial budget. For expenses classified as variable, the accountant calculates the average amount per unit (for manufacturing expenses) or the average amount per sales dollar (for selling, general, and administrative expenses) for each year and then averages these amounts over the three years. The accountant then uses these estimates to project variable costs for the coming year. It is now time to initiate the 2013 budget. Essex's operating results for the last three years were as follows (even though the 2012 year has not ended yet, only two weeks remain and therefore the operating results for the year are available): 2010 2011 2012 Sales in units 80,000 110.000 95,000 Revenues $4,480,000 $6,160,000 $5,320,000 Direct materials $816,000 $1,111,000 $950,000 Direct labor 1.140,000 1.595,000 1,401,250 Plant maintenance 720,000 742,500 736,500 Plant depreciation 420,000 440,000 427,500 Indirect labor 163,200 227,700 193,800 Engineering design 220,000 230,000 240,000 Utilities 81,600 113,300 95,950 Plant administration 325,000 312,500 310,000 Marketing administration 180,000 185,000 190,000 Sales force commissions 134,400 184,800 159,600 Plant supervision 275,000 280,000 300,000 The marketing manager is very optimistic about 2013, and projects the demand for 2013 to be 150,000 fuel pumps. Obviously pleased, Marcy sets about the task of prepar- ing the annual budget for the coming year. Required: a. Classify each of Essex's expenses as being: (1) a variable manufacturing cost; (2) a variable selling cost; (3) a fixed manufacturing cost; or (4) a fixed selling cost b. Using your cost estimates from part (a), what is Essex's budgeted contribution mar- gin income statement for 2013? c. Evaluate the assumptions underlying the budget in light of the unusually optimistic demand projection by the marketing manager