Answered step by step

Verified Expert Solution

Question

1 Approved Answer

8 digit student id = 91234567 Use your 8-digit Student ID as the parameter x, and x, x2, X3, ..., xg as the corresponding entries

8 digit student id = 91234567

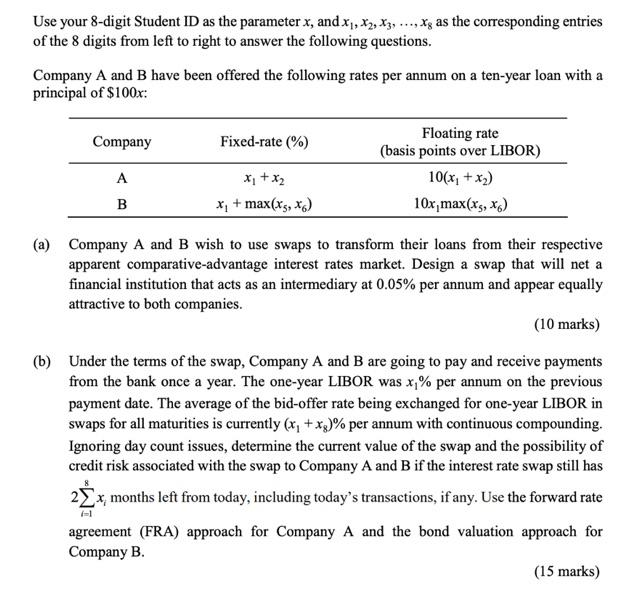

Use your 8-digit Student ID as the parameter x, and x, x2, X3, ..., xg as the corresponding entries of the 8 digits from left to right to answer the following questions. Company A and B have been offered the following rates per annum on a ten-year loan with a principal of $100x: Company A B Fixed-rate (%) x + x x + max(x5, X6) Floating rate (basis points over LIBOR) 10(x + x) 10x, max(x5, X6) (a) Company A and B wish to use swaps to transform their loans from their respective apparent comparative-advantage interest rates market. Design a swap that will net a financial institution that acts as an intermediary at 0.05% per annum and appear equally attractive to both companies. (10 marks) (b) Under the terms of the swap, Company A and B are going to pay and receive payments from the bank once a year. The one-year LIBOR was x% per annum on the previous payment date. The average of the bid-offer rate being exchanged for one-year LIBOR in swaps for all maturities is currently (x+x)% per annum with continuous compounding. Ignoring day count issues, determine the current value of the swap and the possibility of credit risk associated with the swap to Company A and B if the interest rate swap still has 2x, months left from today, including today's transactions, if any. Use the forward rate -1 agreement (FRA) approach for Company A and the bond valuation approach for Company B. (15 marks) Use your 8-digit Student ID as the parameter x, and x, x2, X3, ..., xg as the corresponding entries of the 8 digits from left to right to answer the following questions. Company A and B have been offered the following rates per annum on a ten-year loan with a principal of $100x: Company A B Fixed-rate (%) x + x x + max(x5, X6) Floating rate (basis points over LIBOR) 10(x + x) 10x, max(x5, X6) (a) Company A and B wish to use swaps to transform their loans from their respective apparent comparative-advantage interest rates market. Design a swap that will net a financial institution that acts as an intermediary at 0.05% per annum and appear equally attractive to both companies. (10 marks) (b) Under the terms of the swap, Company A and B are going to pay and receive payments from the bank once a year. The one-year LIBOR was x% per annum on the previous payment date. The average of the bid-offer rate being exchanged for one-year LIBOR in swaps for all maturities is currently (x+x)% per annum with continuous compounding. Ignoring day count issues, determine the current value of the swap and the possibility of credit risk associated with the swap to Company A and B if the interest rate swap still has 2x, months left from today, including today's transactions, if any. Use the forward rate -1 agreement (FRA) approach for Company A and the bond valuation approach for Company B. (15 marks)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance For Non Financial Managers

Authors: Gene Siciliano

1st Edition

0071413774, 978-0071413770