Question: A 2 month put option on the S&P 500 has a strike price of $475. The current value of the index is 485, the

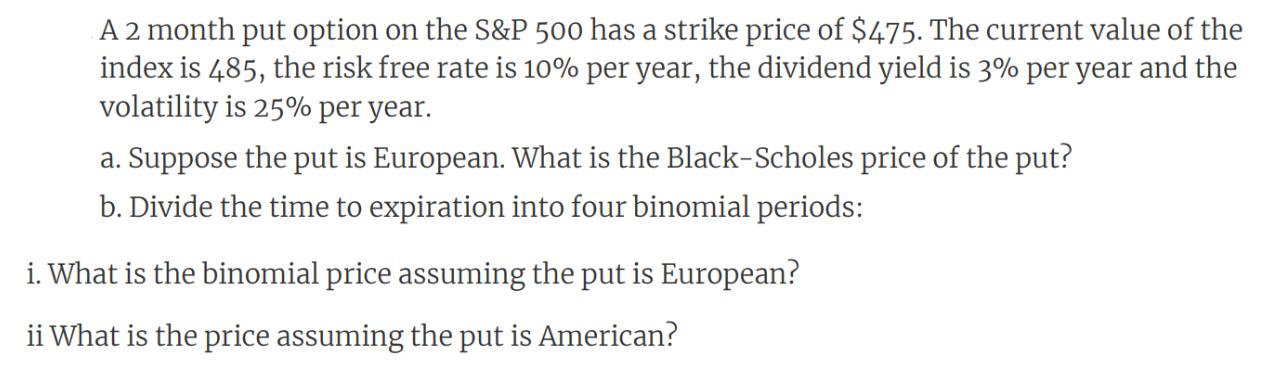

A 2 month put option on the S&P 500 has a strike price of $475. The current value of the index is 485, the risk free rate is 10% per year, the dividend yield is 3% per year and the volatility is 25% per year. a. Suppose the put is European. What is the Black-Scholes price of the put? b. Divide the time to expiration into four binomial periods: i. What is the binomial price assuming the put is European? ii What is the price assuming the put is American?

Step by Step Solution

3.38 Rating (164 Votes )

There are 3 Steps involved in it

a To calculate the BlackScholes price of a European put option we can use the following formula Put ... View full answer

Get step-by-step solutions from verified subject matter experts