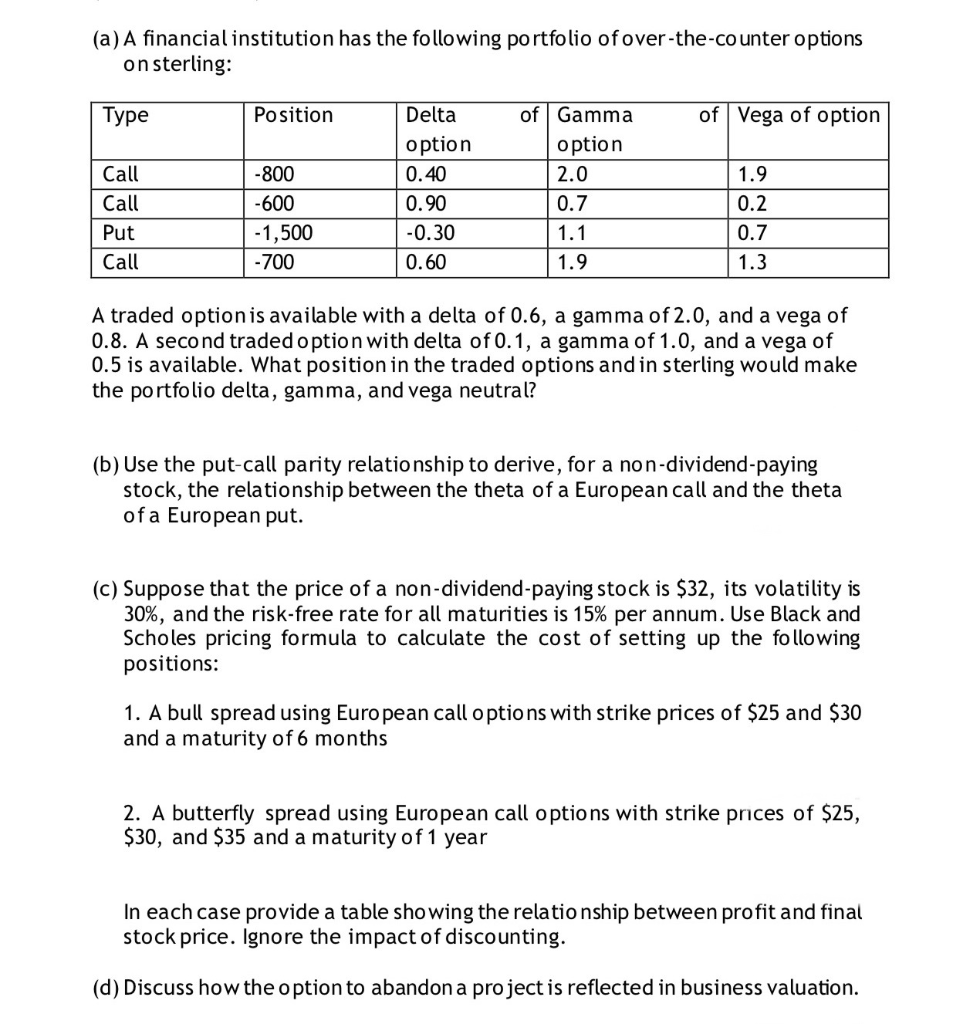

(a) A financial institution has the following portfolio of over-the-counter options on sterling: Type Position of Vega of option Call Call Put Call -800 -600 - 1,500 -700 Delta option 0.40 0.90 -0.30 0.60 of Gamma option 2.0 0.7 1.1 1.9 1.9 0.2 0.7 1.3 A traded option is available with a delta of 0.6, a gamma of 2.0, and a vega of 0.8. A second traded option with delta of 0.1, a gamma of 1.0, and a vega of 0.5 is available. What position in the traded options and in sterling would make the portfolio delta, gamma, and vega neutral? (b) Use the put-call parity relationship to derive, for a non-dividend paying stock, the relationship between the theta of a European call and the theta of a European put. (c) Suppose that the price of a non-dividend-paying stock is $32, its volatility is 30%, and the risk-free rate for all maturities is 15% per annum. Use Black and Scholes pricing formula to calculate the cost of setting up the following positions: 1. A bull spread using European call options with strike prices of $25 and $30 and a maturity of 6 months 2. A butterfly spread using European call options with strike prices of $25, $30, and $35 and a maturity of 1 year In each case provide a table showing the relationship between profit and final stock price. Ignore the impact of discounting. (d) Discuss how the option to abandon a project is reflected in business valuation. (a) A financial institution has the following portfolio of over-the-counter options on sterling: Type Position of Vega of option Call Call Put Call -800 -600 - 1,500 -700 Delta option 0.40 0.90 -0.30 0.60 of Gamma option 2.0 0.7 1.1 1.9 1.9 0.2 0.7 1.3 A traded option is available with a delta of 0.6, a gamma of 2.0, and a vega of 0.8. A second traded option with delta of 0.1, a gamma of 1.0, and a vega of 0.5 is available. What position in the traded options and in sterling would make the portfolio delta, gamma, and vega neutral? (b) Use the put-call parity relationship to derive, for a non-dividend paying stock, the relationship between the theta of a European call and the theta of a European put. (c) Suppose that the price of a non-dividend-paying stock is $32, its volatility is 30%, and the risk-free rate for all maturities is 15% per annum. Use Black and Scholes pricing formula to calculate the cost of setting up the following positions: 1. A bull spread using European call options with strike prices of $25 and $30 and a maturity of 6 months 2. A butterfly spread using European call options with strike prices of $25, $30, and $35 and a maturity of 1 year In each case provide a table showing the relationship between profit and final stock price. Ignore the impact of discounting. (d) Discuss how the option to abandon a project is reflected in business valuation