Answered step by step

Verified Expert Solution

Question

1 Approved Answer

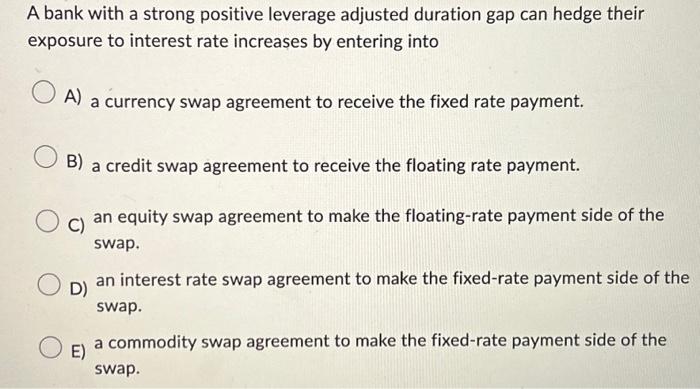

A bank with a strong positive leverage adjusted duration gap can hedge their exposure to interest rate increases by entering into O A) a currency

A bank with a strong positive leverage adjusted duration gap can hedge their exposure to interest rate increases by entering into O A) a currency swap agreement to receive the fixed rate payment. B) a credit swap agreement to receive the floating rate payment. C) an equity swap agreement to make the floating-rate payment side of the swap. D) an interest rate swap agreement to make the fixed-rate payment side of the swap. E) a commodity swap agreement to make the fixed-rate payment side of the swap.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Regulation A+ And Other Alternatives To A Traditional IPO Financing Your Growth Business Following The JOBS Act

Authors: David N. Feldman

1st Edition

1119416159,1119416124