Answered step by step

Verified Expert Solution

Question

1 Approved Answer

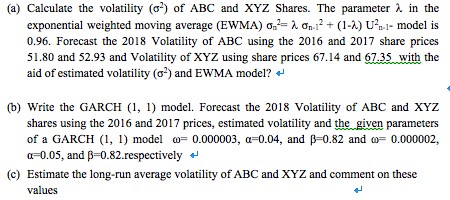

(a) Calculate the volatility (P) of ABC and XYZ Shares. The parameter ? in the exponential weighted moving average (EWMA) ?-? ??.2+ (1-A) Uar model

(a) Calculate the volatility (P) of ABC and XYZ Shares. The parameter ? in the exponential weighted moving average (EWMA) ?-? ??.2+ (1-A) Uar model is 0.96. Forecast the 2018 Volatility of ABC using the 2016 and 2017 share prices 51.80 and 52.93 and Volatility of XYZ using share prices 67.14 and 67.35 with the aid of estimated volatility (o2) and EWMA model? (b) Write the GARCH 1) model. Forecast the 2018 Volatility of ABC and XYZ shares using the 2016 and 2017 prices, estimated volatility and the given parameters of a GARCH (, 1) modelo0.000003, a-0.04, and p-0.82 and o- 0.000002, 0.05, and p-0.82.respectively +' (c) Estimate the long-run average volatility of ABC and XYZ and comment on these values

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bitcoin A Beginner S Guide

Authors: Benjamin Hart

1st Edition

0578389533, 978-0578389530