Answered step by step

Verified Expert Solution

Question

1 Approved Answer

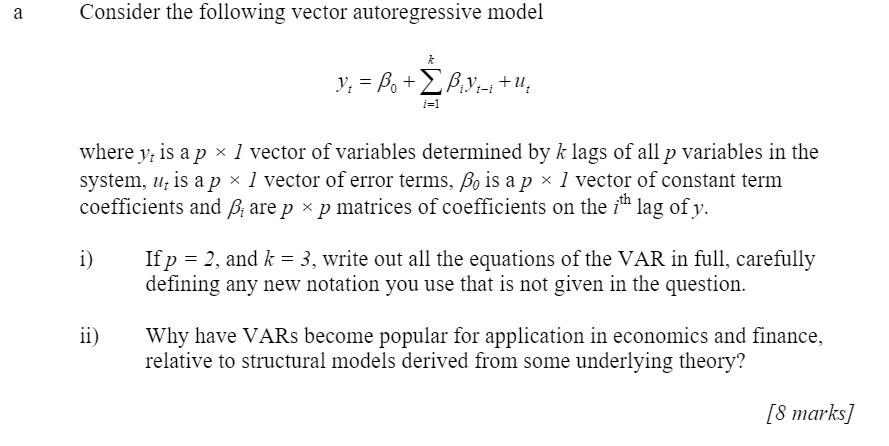

a Consider the following vector autoregressive model k y = Po +By+U i=1 where y, is a px 1 vector of variables determined by

a Consider the following vector autoregressive model k y = Po +By+U i=1 where y, is a px 1 vector of variables determined by k lags of all p variables in the system, ut is a px 1 vector of error terms, po is a p 1 vector of constant term coefficients and ; are p p matrices of coefficients on the ith lag of y. i) ii) If p = 2, and k = 3, write out all the equations of the VAR in full, carefully defining any new notation you use that is not given in the question. Why have VARS become popular for application in economics and finance, relative to structural models derived from some underlying theory? [8 marks]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding financial statements

Authors: Lyn M. Fraser, Aileen Ormiston

9th Edition

136086241, 978-0136086246