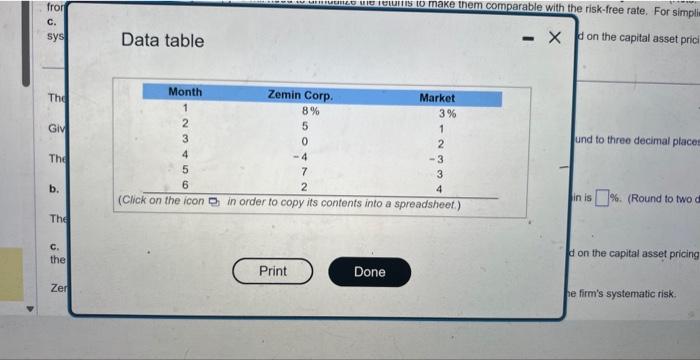

a. Given the following holding-period returns, , compute the average returns and the standard deviations for the Zemin Corporation and for the market. b. If Zemin's beta is 1.93 and the risk-free rate is 9 percent, what would be an expected return for an investor owning Zemin? (Note- Because the preceding returns are based on monthly data, you will need to annualize the returns to make them comparable with the risk-free rafe, For simplicity, you can convert from monthly to yearly retums by multiplying the averago monthly returns by 12.) c. How does Zemin's historical average retum compare with the return you believe you should expect based on the capital asset pricing model and the firm's systematic risk? a. Given the holding period returns shown in the table, the average monthly return for the Zemin Corporation is 4. (Round to two decimal places) The standard deviation for the Zemin Corporation is \%. (Round to two decimal placess.) Given the holding-period returns shown in the table, the average monthly return for the market is \%. (Round to three decimal places.) The standard deviation for the market is \%. (Round to two decimal places.) b. If Zemin's beta is 1.93 and the risk-free rate is 9 percent, the expected retum for an investor owning Zemin is \%. (Round to two decinal places.) The average annuat historical return for Zernin is \%. (Round to two decimal places:) c. How does Zernin's historical average relum compare with the return you believe you should expect based on the capital asset pricing model and the firm's systematic risk? (Select from the drop-down menu.) a. Given the following holding-period returns, . compute the average roturns and the standard deviations for the Zemin Corporation and for the makat. b. If Zemin's beta is 1.93 and the risk-free rate is 9 percent. What would be an expected return for an investor owning Zemin? (Note: Because the preceding returns are based on monthy data, you will need to annualize the returns to make them comparablo with the risk-free rate. For simplicity. you can convert from monthly to yearly returns by multiplying the average monthy retuins by 12.) c. How does Zomin's historical average return compare with the return you beliove you should expect based on the captal asset pricing model and the firm's systematic risk? The standard deviation for the Zemin Corporation is \%. (Round to two decimal places.) Given the holding-period returns shown in the table, the average monthly return for the market is \%. (Round to three decimal places.) The standard deviation for the market is of. (Round to two decimal places.) b. If Zemin's beta is 1.93 and the ril the expected retum for an investor owning Zemin is \%. (Round to two decimal places.) The average annual historical returr ind to two decimal places.) c. How does Zemin's historical aveil the firm's systematic risk? (Select f ithe retum you believe you should expect based on the capital asset pricing modet and ) Zemin's historical average return is the retum based on the capital asset pricing model and the firm's systematic risk. Data table