Answered step by step

Verified Expert Solution

Question

1 Approved Answer

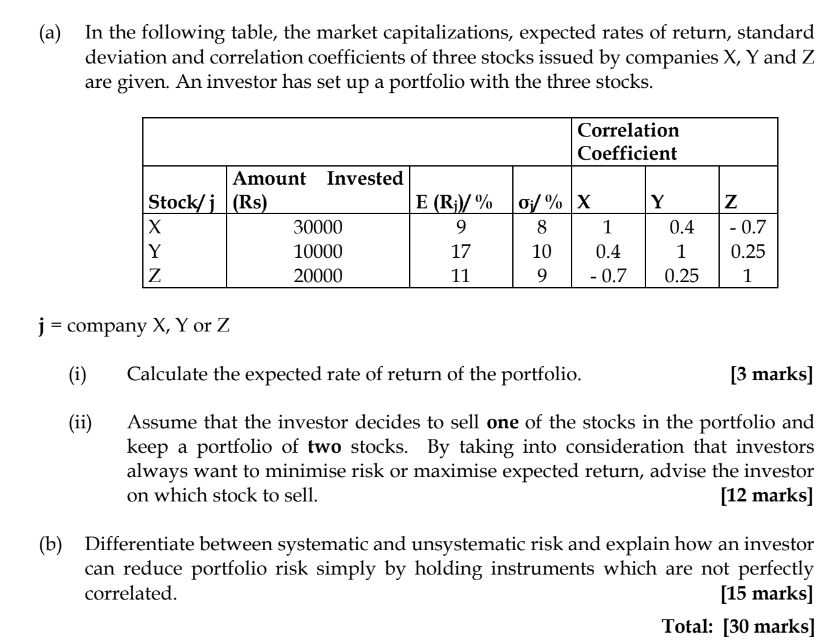

(a) In the following table, the market capitalizations, expected rates of return, standard deviation and correlation coefficients of three stocks issued by companies X, Y

(a) In the following table, the market capitalizations, expected rates of return, standard deviation and correlation coefficients of three stocks issued by companies X, Y and Z are given. An investor has set up a portfolio with the three stocks. j=companyX,YorZ (i) Calculate the expected rate of return of the portfolio. [3 marks] (ii) Assume that the investor decides to sell one of the stocks in the portfolio and keep a portfolio of two stocks. By taking into consideration that investors always want to minimise risk or maximise expected return, advise the investor on which stock to sell. [12 marks] (b) Differentiate between systematic and unsystematic risk and explain how an investor can reduce portfolio risk simply by holding instruments which are not perfectly correlated. [15 marks]

(a) In the following table, the market capitalizations, expected rates of return, standard deviation and correlation coefficients of three stocks issued by companies X, Y and Z are given. An investor has set up a portfolio with the three stocks. j=companyX,YorZ (i) Calculate the expected rate of return of the portfolio. [3 marks] (ii) Assume that the investor decides to sell one of the stocks in the portfolio and keep a portfolio of two stocks. By taking into consideration that investors always want to minimise risk or maximise expected return, advise the investor on which stock to sell. [12 marks] (b) Differentiate between systematic and unsystematic risk and explain how an investor can reduce portfolio risk simply by holding instruments which are not perfectly correlated. [15 marks] Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Municipal Budget Crunch A Handbook For Professionals

Authors: Roger L. Kemp

1st Edition

0786463740, 978-0786463749