Question

A) Last year, you borrowed $8,000 from a bank and agreed to a repayment plan of paying an equal amount over 6 years. This year,

A) Last year, you borrowed $8,000 from a bank and agreed to a repayment plan of paying an equal amount over 6 years. This year, right after making your first payment, you win a lottery, so want to get out of the loan now by paying the remaining balance. How much balance do you need to pay? Suppose that the interest rate is 5%.

B) You are considering making a portfolio using stock A and risk-free asset. The expected return on A is 12% and its standard deviation is 20%. The risk-free rate is 4%. If you want the standard deviation of portfolio return to be not greater than 15%, what is the highest expected return you can earn from the portfolio? (3 points)

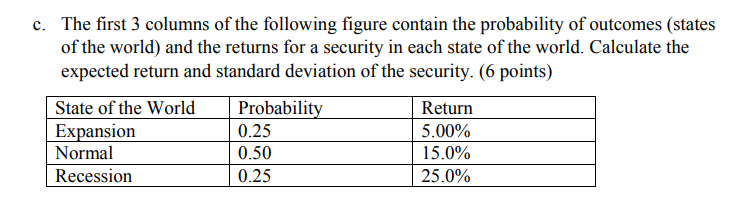

c. The first 3 columns of the following figure contain the probability of outcomes (states of the world, and the returns for a security in each state of the world. Calculate the expected return and standard deviation of the security. (6 points) State of the World Probability Return Expansion 0.25 5.00% Normal 0.50 15.0% Recession 0.25 25.0%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Key Financial Market Concepts

Authors: Bob Steiner

2nd Edition

0273750127, 978-0273750123