Answered step by step

Verified Expert Solution

Question

1 Approved Answer

A major Australian bank has assets of $29 billion. After applying the regulator-stipulated risk weightings, the institution estimates total risk-weighted assets of $6.01 billion. Assuming

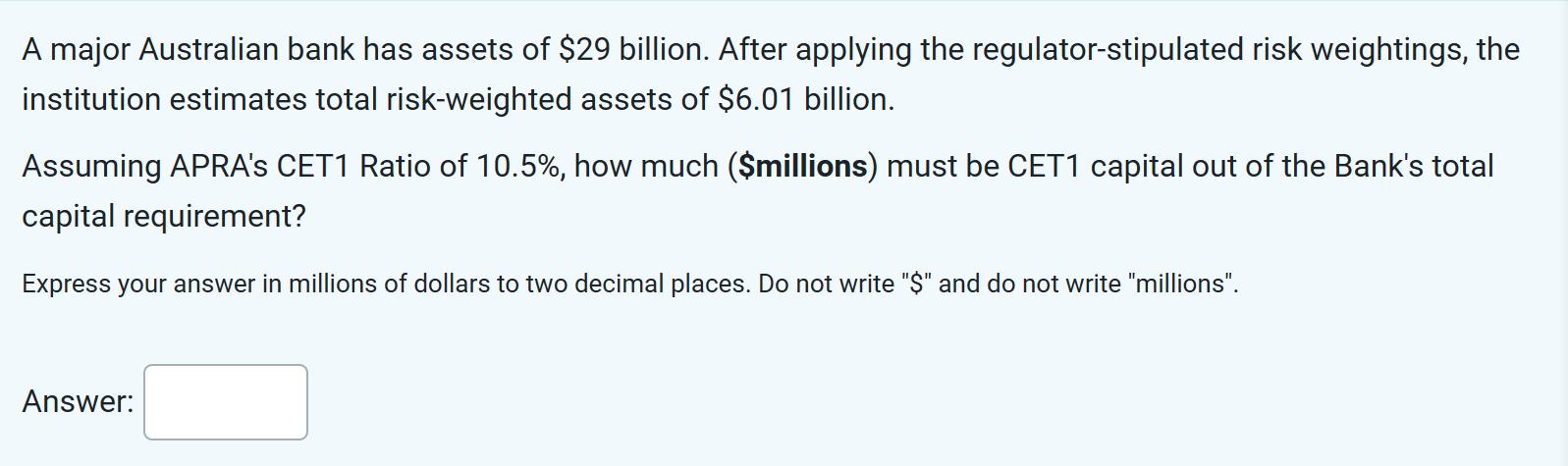

A major Australian bank has assets of $29 billion. After applying the regulator-stipulated risk weightings, the institution estimates total risk-weighted assets of $6.01 billion. Assuming APRA's CET1 Ratio of 10.5\%, how much (\$millions) must be CET1 capital out of the Bank's total capital requirement? Express your answer in millions of dollars to two decimal places. Do not write "\$" and do not write "millions

A major Australian bank has assets of $29 billion. After applying the regulator-stipulated risk weightings, the institution estimates total risk-weighted assets of $6.01 billion. Assuming APRA's CET1 Ratio of 10.5\%, how much (\$millions) must be CET1 capital out of the Bank's total capital requirement? Express your answer in millions of dollars to two decimal places. Do not write "\$" and do not write "millions Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Market Regulations And Finance

Authors: Ratan Khasnabis, Indrani Chakraborty

2014th Edition

8132217942, 978-8132217947