Answered step by step

Verified Expert Solution

Question

1 Approved Answer

a. Record the preceding events in a horizontal statements model. The first row shows beginning balances. b. Record the entry to close the amount of

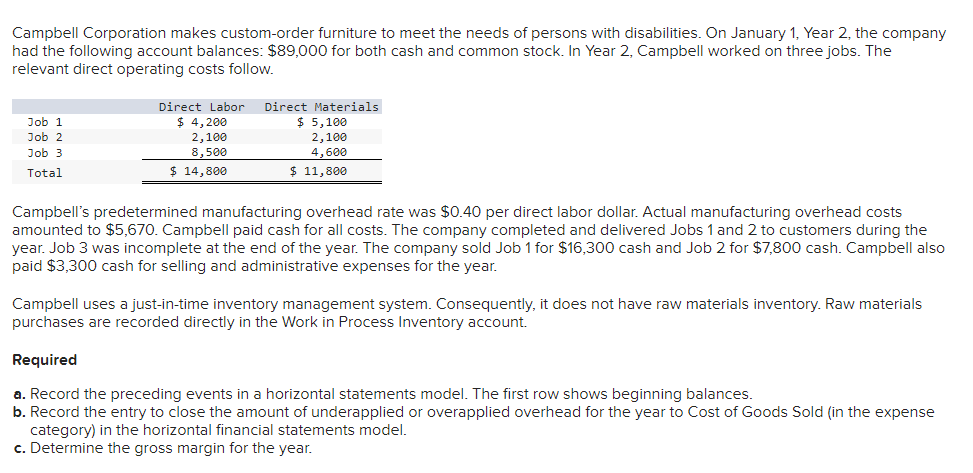

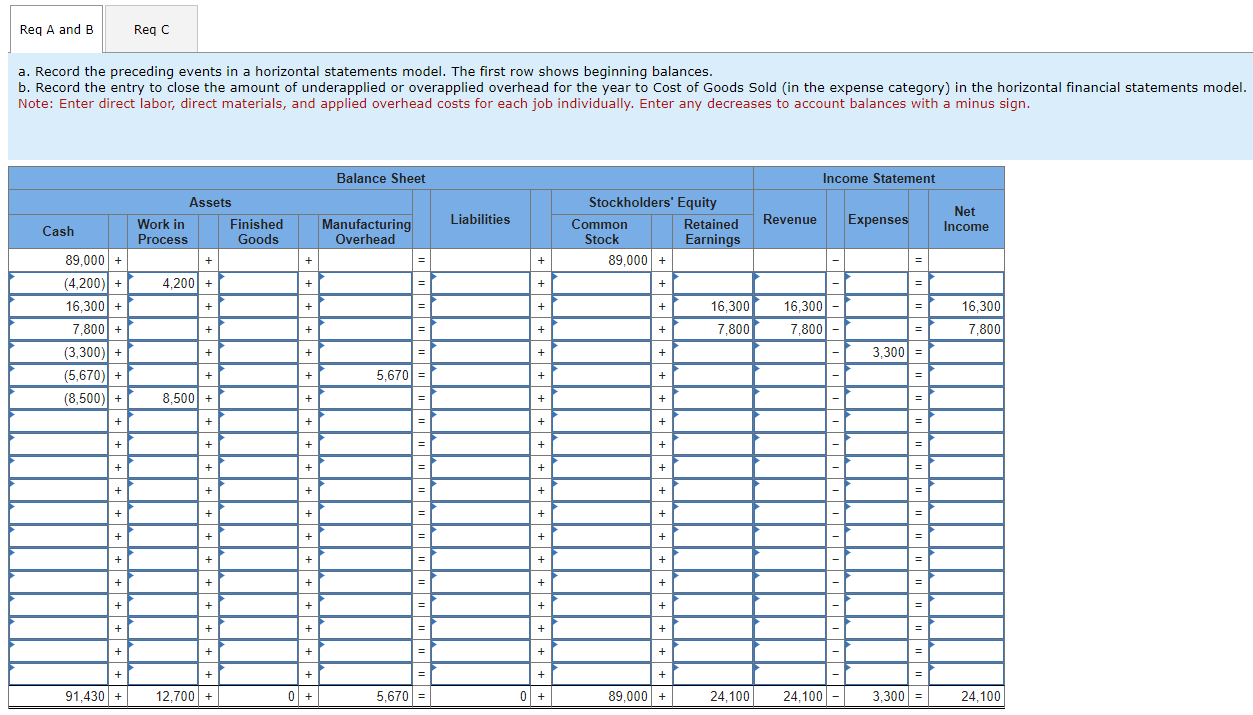

a. Record the preceding events in a horizontal statements model. The first row shows beginning balances. b. Record the entry to close the amount of underapplied or overapplied overhead for the year to Cost of Goods Sold (in the expense category) in the horizontal financial statements model. Note: Enter direct labor, direct materials, and applied overhead costs for each job individually. Enter any decreases to account balances with a minus sign. Determine the gross margin for the year. Campbell Corporation makes custom-order furniture to meet the needs of persons with disabilities. On January 1, Year 2, the company had the following account balances: $89,000 for both cash and common stock. In Year 2, Campbell worked on three jobs. The relevant direct operating costs follow. Campbell's predetermined manufacturing overhead rate was $0.40 per direct labor dollar. Actual manufacturing overhead costs amounted to $5,670. Campbell paid cash for all costs. The company completed and delivered Jobs 1 and 2 to customers during the year. Job 3 was incomplete at the end of the year. The company sold Job 1 for $16,300 cash and Job 2 for $7,800 cash. Campbell also paid $3,300 cash for selling and administrative expenses for the year. Campbell uses a just-in-time inventory management system. Consequently, it does not have raw materials inventory. Raw materials purchases are recorded directly in the Work in Process Inventory account. Required a. Record the preceding events in a horizontal statements model. The first row shows beginning balances. b. Record the entry to close the amount of underapplied or overapplied overhead for the year to Cost of Goods Sold (in the expense category) in the horizontal financial statements model. c. Determine the gross margin for the year

a. Record the preceding events in a horizontal statements model. The first row shows beginning balances. b. Record the entry to close the amount of underapplied or overapplied overhead for the year to Cost of Goods Sold (in the expense category) in the horizontal financial statements model. Note: Enter direct labor, direct materials, and applied overhead costs for each job individually. Enter any decreases to account balances with a minus sign. Determine the gross margin for the year. Campbell Corporation makes custom-order furniture to meet the needs of persons with disabilities. On January 1, Year 2, the company had the following account balances: $89,000 for both cash and common stock. In Year 2, Campbell worked on three jobs. The relevant direct operating costs follow. Campbell's predetermined manufacturing overhead rate was $0.40 per direct labor dollar. Actual manufacturing overhead costs amounted to $5,670. Campbell paid cash for all costs. The company completed and delivered Jobs 1 and 2 to customers during the year. Job 3 was incomplete at the end of the year. The company sold Job 1 for $16,300 cash and Job 2 for $7,800 cash. Campbell also paid $3,300 cash for selling and administrative expenses for the year. Campbell uses a just-in-time inventory management system. Consequently, it does not have raw materials inventory. Raw materials purchases are recorded directly in the Work in Process Inventory account. Required a. Record the preceding events in a horizontal statements model. The first row shows beginning balances. b. Record the entry to close the amount of underapplied or overapplied overhead for the year to Cost of Goods Sold (in the expense category) in the horizontal financial statements model. c. Determine the gross margin for the year Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Auditing And Other Assurance Services

Authors: Ray Whittington, Kurt Pany

16th Edition

007352686X, 978-0073526867