Question

A trader has entered into a forward rate agreement in which it will receive 4.5% based on quarterly compounding for a three-month period starting in

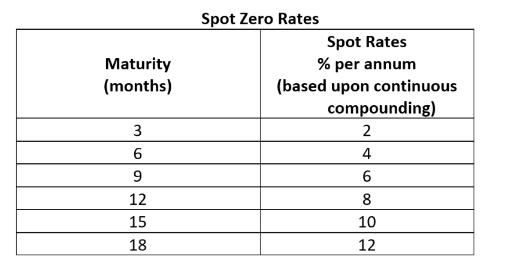

A trader has entered into a forward rate agreement in which it will receive 4.5% based on quarterly compounding for a three-month period starting in 9 months. The notional value of the forward rate agreement is $10,000,000. Note that the spot zero rates in the table below are based upon continuous compounding.

a. Given the data below, what is the value of a forward rate agreement?

b. Provide two ways in which the trader can hedge the risk of the forward rate agreement?

Spot Zero Rates Spot Rates % per annum Maturity (based upon continuous compounding) (months) 3 2 4 12 8 15 10 18 12

Step by Step Solution

3.40 Rating (162 Votes )

There are 3 Steps involved in it

Step: 1

The 9 months period will start after three months It means it will be 12 months time from now onw...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Markets and Institutions

Authors: Anthony Saunders, Marcia Cornett

6th edition

9780077641849, 77861663, 77641841, 978-0077861667