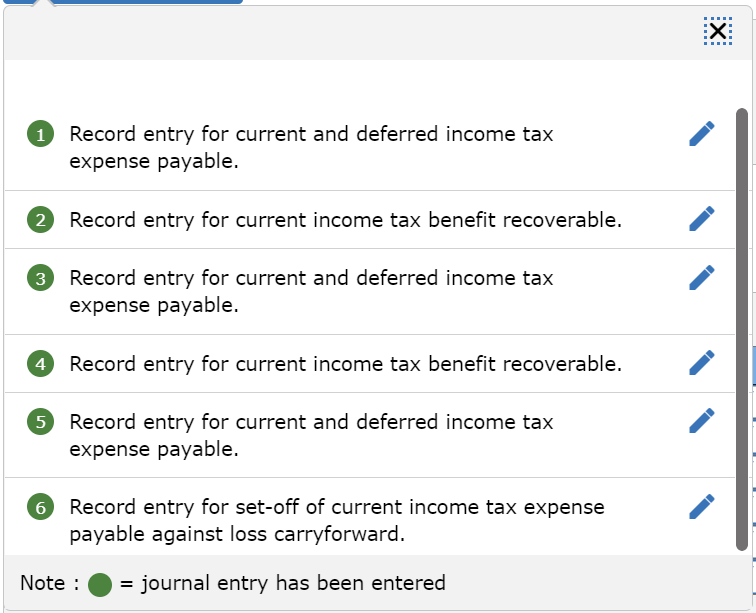

A17-18 Loss Carryback/Carryforward; Temporary Differences; Rate Change (LO 17-4) On 1 January 20X4, Dart Incorporated commenced business operations. The following information is available to you: Earnings (loss) before tax Tax rate (enacted in each year) Depreciation (original cost of assets, $1,000,000) Capital cost allowance Rental revenue recognized* 20X4 $90,000 36% 50,000 60,000 60,000 20X5 $(410,000) 36% 50,000 0 20x6 $100,000 32% 50,000 120,000 20X7 $120,000 30% 50,000 110,000 *There is a rent receivable account at the end of 20X4, because rent revenue was earned in 20X4 but will not be collected until 20X6. This amount is not part of taxable income in 20X4, but will be taxable income in 20x6 when it is collected. Required: Prepare journal entries to record tax for 20X4, 20X5, 20X6, and 20x7. Assume that the tax loss carryforward usage in 20X5 is considered to be not probable but that in 20x6 the balance of probability shifts and in 20X6 the loss usage is considered to be probable. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) :X: 1 Record entry for current and deferred income tax expense payable. Record entry for current income tax benefit recoverable. Record entry for current and deferred income tax expense payable. Record entry for current income tax benefit recoverable. Record entry for current and deferred income tax expense payable. Record entry for set-off of current income tax expense payable against loss carryforward. Note : = journal entry has been entered View transaction list View journal entry worksheet No Date General Journal Debit Credit 1 20X4 32,400 Income tax expense Deferred income tax 25,200 7,200 Tax payable 2 20X5 Tax receivable 7,200 18,000 Deferred income tax Income tax expense (recovery) 25,200 3 20X6 Income tax expense Deferred income tax Tax payable 28,800 4 20X6 Tax payable 28,880 Deferred income tax Income tax expense (recovery) 5 20X7 Income tax expense Deferred income tax Tax payable 18,000 6 20X7 Tax payable 18,000 Income tax expense Deferred income tax A17-18 Loss Carryback/Carryforward; Temporary Differences; Rate Change (LO 17-4) On 1 January 20X4, Dart Incorporated commenced business operations. The following information is available to you: Earnings (loss) before tax Tax rate (enacted in each year) Depreciation (original cost of assets, $1,000,000) Capital cost allowance Rental revenue recognized* 20X4 $90,000 36% 50,000 60,000 60,000 20X5 $(410,000) 36% 50,000 0 20x6 $100,000 32% 50,000 120,000 20X7 $120,000 30% 50,000 110,000 *There is a rent receivable account at the end of 20X4, because rent revenue was earned in 20X4 but will not be collected until 20X6. This amount is not part of taxable income in 20X4, but will be taxable income in 20x6 when it is collected. Required: Prepare journal entries to record tax for 20X4, 20X5, 20X6, and 20x7. Assume that the tax loss carryforward usage in 20X5 is considered to be not probable but that in 20x6 the balance of probability shifts and in 20X6 the loss usage is considered to be probable. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) :X: 1 Record entry for current and deferred income tax expense payable. Record entry for current income tax benefit recoverable. Record entry for current and deferred income tax expense payable. Record entry for current income tax benefit recoverable. Record entry for current and deferred income tax expense payable. Record entry for set-off of current income tax expense payable against loss carryforward. Note : = journal entry has been entered View transaction list View journal entry worksheet No Date General Journal Debit Credit 1 20X4 32,400 Income tax expense Deferred income tax 25,200 7,200 Tax payable 2 20X5 Tax receivable 7,200 18,000 Deferred income tax Income tax expense (recovery) 25,200 3 20X6 Income tax expense Deferred income tax Tax payable 28,800 4 20X6 Tax payable 28,880 Deferred income tax Income tax expense (recovery) 5 20X7 Income tax expense Deferred income tax Tax payable 18,000 6 20X7 Tax payable 18,000 Income tax expense Deferred income tax