Answered step by step

Verified Expert Solution

Question

1 Approved Answer

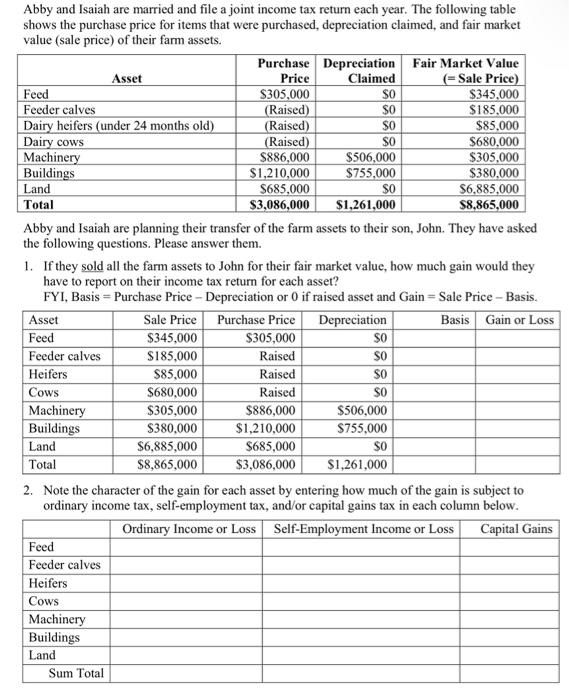

Abby and Isaiah are married and file a joint income tax return each year. The following table shows the purchase price for items that were

Abby and Isaiah are married and file a joint income tax return each year. The following table shows the purchase price for items that were purchased, depreciation claimed, and fair market value (sale price) of their farm assets.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Information Audit A Practical Guide

Authors: Susan Henczel, Sue Henczel

1st Edition

3598243677, 978-3598243677