Answered step by step

Verified Expert Solution

Question

1 Approved Answer

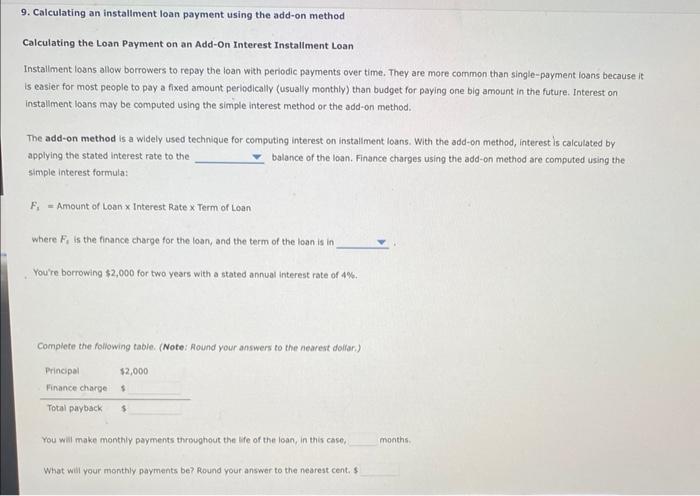

9. Calculating an installment loan payment using the add-on method Calculating the Loan Payment on an Add-On Interest Installment Loan Installment loans allow borrowers

9. Calculating an installment loan payment using the add-on method Calculating the Loan Payment on an Add-On Interest Installment Loan Installment loans allow borrowers to repay the loan with periodic payments over time. They are more common than single-payment loans because it is easier for most people to pay a fixed amount periodically (usually monthly) than budget for paying one big amount in the future. Interest on installment loans may be computed using the simple interest method or the add-on method. The add-on method is a widely used technique for computing interest on installment loans. With the add-on method, interest is calculated by applying the stated interest rate to the balance of the loan. Finance charges using the add-on method are computed using the simple interest formula: F - Amount of Loan x Interest Rate x Term of Loan where F, is the finance charge for the loan, and the term of the loan is in You're borrowing $2,000 for two years with a stated annual interest rate of 4%. Complete the following table. (Note: Round your answers to the nearest dollar) Principal Finance charge $ Total payback $ $2,000 You will make monthly payments throughout the life of the loan, in this case, What will your monthly payments be? Round your answer to the nearest cent. $ months.

Step by Step Solution

★★★★★

3.50 Rating (160 Votes )

There are 3 Steps involved in it

Step: 1

Question 1 With the addon method interest is calcu...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamental Accounting Principles

Authors: John J. Wild, Ken W. Shaw, Barbara Chiappetta

20th Edition

1259157148, 78110874, 9780077616212, 978-1259157141, 77616219, 978-0078110870