Answered step by step

Verified Expert Solution

Question

1 Approved Answer

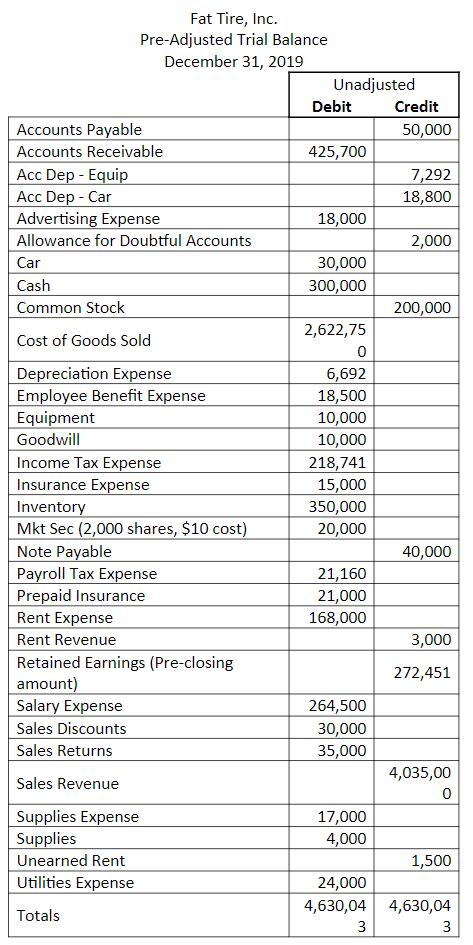

The financial statements will cover the year ended December 31, 2019. I printed out the most current unadjusted trial balance below. Many of these

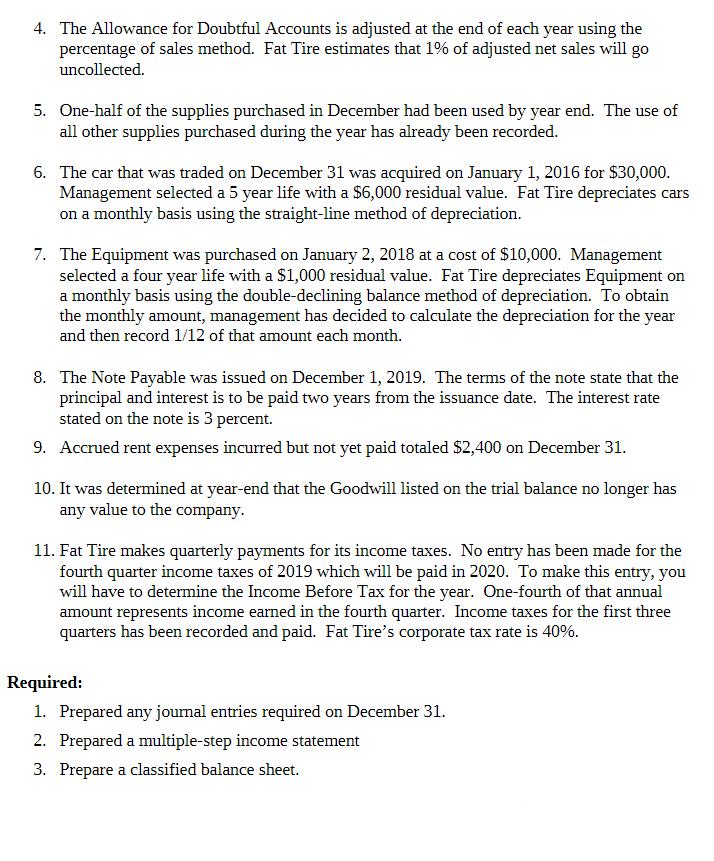

The financial statements will cover the year ended December 31, 2019. I printed out the most current unadjusted trial balance below. Many of these balances will change based on the remaining journal entries that need to be recorded for December 31. You will also have to add some accounts as adjusting entries are recorded. Information needed to record the remaining entries follow this unadjusted trial balance. Accounts Payable Accounts Receivable Acc Dep - Equip Acc Dep - Car Fat Tire, Inc. Pre-Adjusted Trial Balance December 31, 2019 Advertising Expense Allowance for Doubtful Accounts Car Cash Common Stock Cost of Goods Sold Depreciation Expense Employee Benefit Expense Equipment Goodwill Income Tax Expense Insurance Expense Inventory Mkt Sec (2,000 shares, $10 cost) Note Payable Payroll Tax Expense Prepaid Insurance Rent Expense Rent Revenue Retained Earnings (Pre-closing amount) Salary Expense Sales Discounts Sales Returns Sales Revenue Supplies Expense Supplies Unearned Rent Utilities Expense Totals Unadjusted Debit 425,700 18,000 30,000 300,000 2,622,75 0 6,692 18,500 10,000 10,000 218,741 15,000 350,000 20,000 21,160 21,000 168,000 264,500 30,000 35,000 17,000 4,000 24,000 4,630,04 3 Credit 50,000 7,292 18,800 2,000 200,000 40,000 3,000 272,451 4,035,00 0 1,500 4,630,04 3 Transactions that occurred on December 31 that have not been recorded: a. The Marketable Securities shown on the trial balance represent 2,000 shares of another company's stock that were purchased on December 5th at $10 per share. On December 31, 1,500 of these shares were sold at the December 31 closing market price of $12 per share. No entries have been made since the securities were acquired. b. Received cash dividends from the Marketable Securities on December totaling $150. c. A sales return that occurred on December 31 needs to be recorded. The sales price was $1,200 and the cost of goods sold was $450. All sales are on account. d. Brent was able to get a special New Year's Eve deal on a trade of the company car. The new car price was $35,000. Brent was able to get a $10,000 trade-in allowance on the old car. We paid cash for the difference. The trade has not been recorded. The effective date of the trade was December 31. Information related to depreciation of the old car is listed below in item (6). Other information related to adjusting entries: 1. Information for the last pay period of the year is below. Cash will not change hands for this pay period until January of 2020. The salaries, related payroll tax expenses, and related employee benefit expenses have been incurred but not yet recorded. Gross Pay = $11,500 Federal Income Tax withholding rate = 20% FICA rate for employees and employers = 8% for each Medical Insurance Premiums withheld from employees = $500 Employer's share of Medical Insurance Premiums = $400 401K withheld from employees = $575 Employer's match on 401K = $345 State unemployment taxes for the pay period = $300 Federal unemployment taxes for the pay period = $100 Fat Tire maintains a separate account for each payroll related liability on its Balance Sheet. Do not worry about any wage base limits. 2. The Prepaid Insurance balance represents a $36,000 one-year policy that began on July 1. The company adjusts any prepaid items on a monthly basis. 3. Fat Tire decided to sublease some of its rental space. On October 1, the company received $4,500 in advance from a neighboring business for 3 month's rent. The lease period began on October 1. Fat Tire adjusts rent related accounts on a monthly basis. 4. The Allowance for Doubtful Accounts is adjusted at the end of each year using the percentage of sales method. Fat Tire estimates that 1% of adjusted net sales will go uncollected. 5. One-half of the supplies purchased in December had been used by year end. The use of all other supplies purchased during the year has already been recorded. 6. The car that was traded on December 31 was acquired on January 1, 2016 for $30,000. Management selected a 5 year life with a $6,000 residual value. Fat Tire depreciates cars on a monthly basis using the straight-line method of depreciation. 7. The Equipment was purchased on January 2, 2018 at a cost of $10,000. Management selected a four year life with a $1,000 residual value. Fat Tire depreciates Equipment on a monthly basis using the double-declining balance method of depreciation. To obtain the monthly amount, management has decided to calculate the depreciation for the year and then record 1/12 of that amount each month. 8. The Note Payable was issued on December 1, 2019. The terms of the note state that the principal and interest is to be paid two years from the issuance date. The interest rate stated on the note is 3 percent. 9. Accrued rent expenses incurred but not yet paid totaled $2,400 on December 31. 10. It was determined at year-end that the Goodwill listed on the trial balance no longer has any value to the company. 11. Fat Tire makes quarterly payments for its income taxes. No entry has been made for the fourth quarter income taxes of 2019 which will be paid in 2020. To make this entry, you will have to determine the Income Before Tax for the year. One-fourth of that annual amount represents income earned in the fourth quarter. Income taxes for the first three quarters has been recorded and paid. Fat Tire's corporate tax rate is 40%. Required: 1. Prepared any journal entries required on December 31. 2. Prepared a multiple-step income statement 3. Prepare a classified balance sheet.

Step by Step Solution

★★★★★

3.42 Rating (152 Votes )

There are 3 Steps involved in it

Step: 1

Answer Solution Journal Entries Particulars Dr Cr Cash accounts 121500 18000 Marketable securities 101500 15000 profit on sale of securities balance 3...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Accounting

Authors: Floyd A. Beams, Joseph H. Anthony, Bruce Bettinghaus, Kenneth Smith

13th edition

134472144, 978-0134472140