Answered step by step

Verified Expert Solution

Question

1 Approved Answer

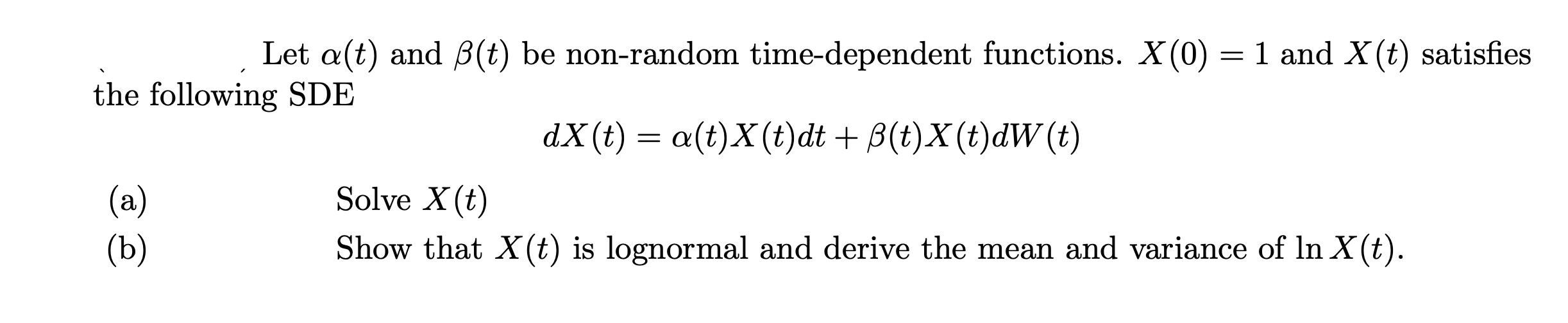

Let a(t) and B(t) be non-random time-dependent functions. X(0) = 1 and X(t) satisfies the following SDE dX(t) = a(t)X(t)dt + (t)X(t)dW (t) (a)

Let a(t) and B(t) be non-random time-dependent functions. X(0) = 1 and X(t) satisfies the following SDE dX(t) = a(t)X(t)dt + (t)X(t)dW (t) (a) (b) Solve X(t) Show that X(t) is lognormal and derive the mean and variance of In X(t).

Step by Step Solution

★★★★★

3.40 Rating (144 Votes )

There are 3 Steps involved in it

Step: 1

By letting X t be the solution to the S DE ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: Jerry J. Weygandt, Paul D. Kimmel, Donald E. Kieso

IFRS 3rd edition

1118978080, 978-1119153726, 1119153727, 978-1119153702, 978-1118978085