Answered step by step

Verified Expert Solution

Question

1 Approved Answer

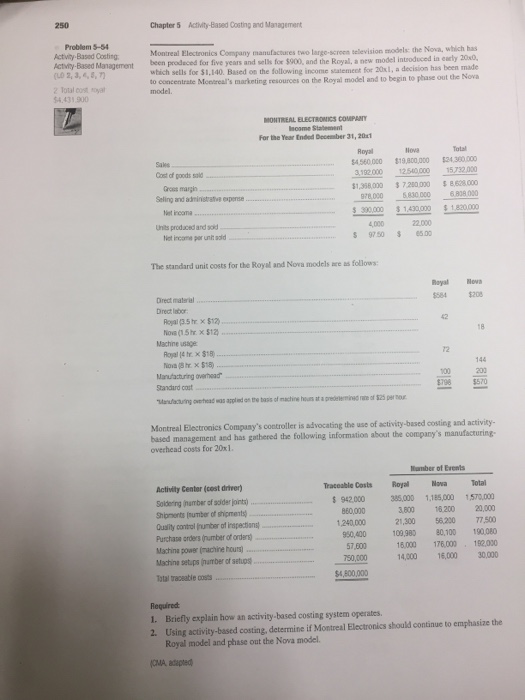

Activity based costing 250 Chapter 5 Activity-Based Costing and Management Problem 5-54 ctivity Based Costing Actvity-Based Managementb Montreal Electronics Company manufactures two large-scroen television models:

Activity based costing

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

IT Auditing Using A System Perspective Premier Reference Source

Authors: Robert Elliot Davis

1st Edition

1799855481, 978-1799855484