Answered step by step

Verified Expert Solution

Question

1 Approved Answer

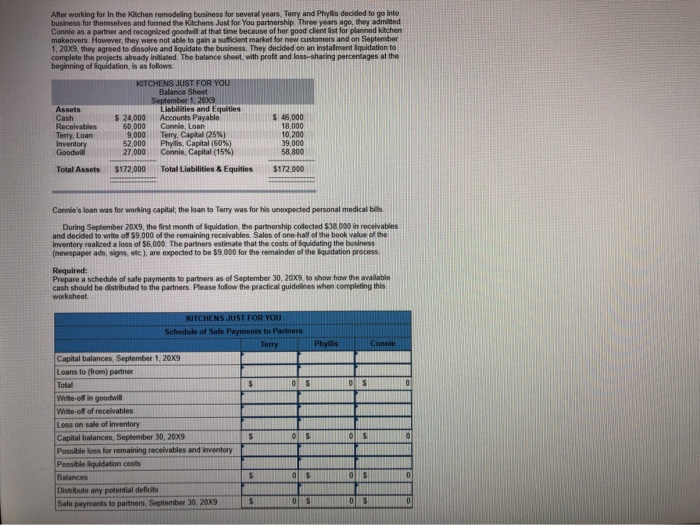

After working for In the Kitchen remodeling business for several years, Temry and Phyllis decided to go into business for themselves and formed the Kitchens

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

NHS Audit Committee Handbook Practical Guides

Authors: Governance And Audit Committee

3rd Edition

1904624839, 978-1904624837