Answered step by step

Verified Expert Solution

Question

1 Approved Answer

All parts in this problem are under the setting of Black-Litterman model. Assume the risk-free rate is 0% under all parts. (a). Suppose there are

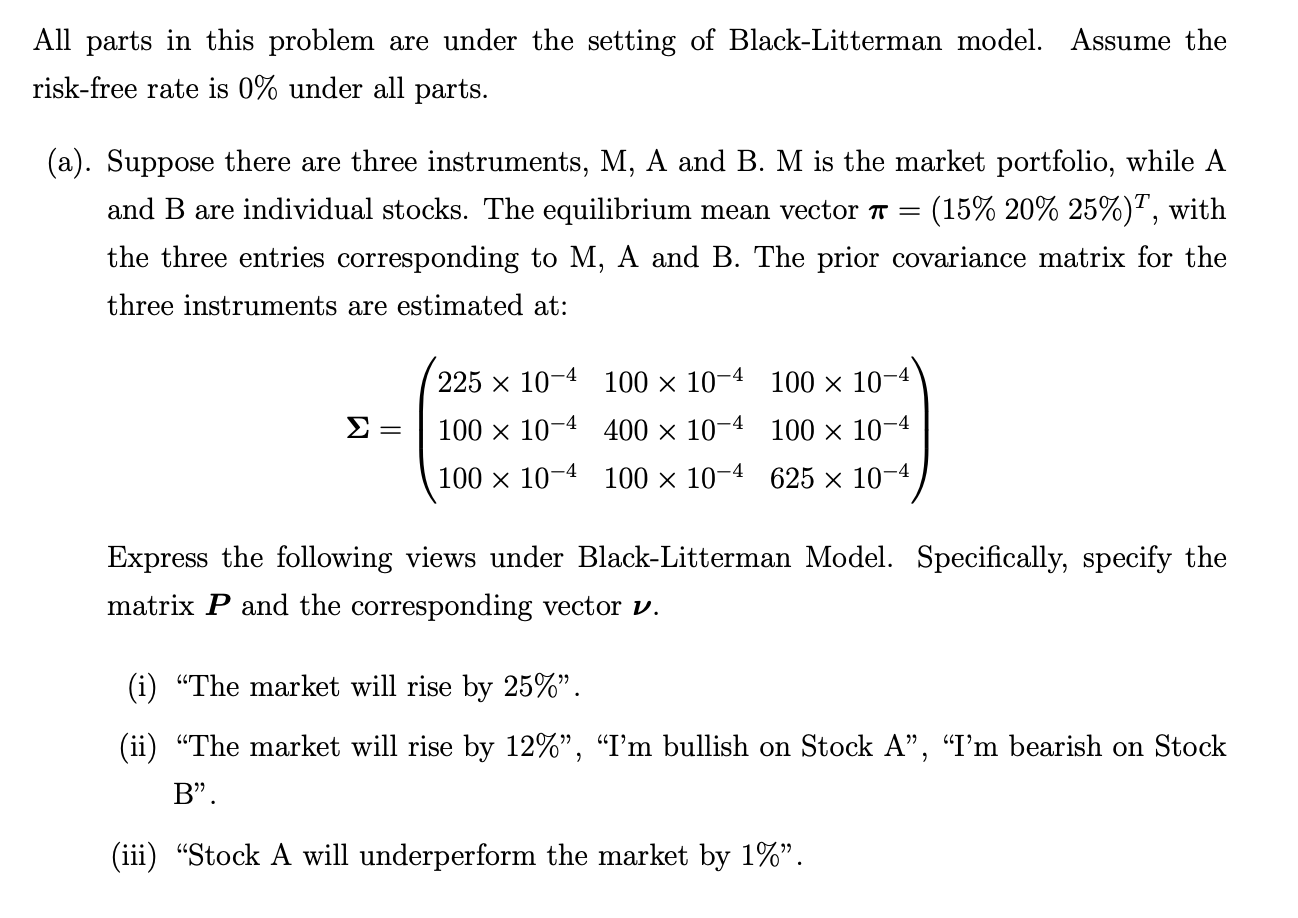

All parts in this problem are under the setting of Black-Litterman model. Assume the risk-free rate is 0% under all parts. (a). Suppose there are three instruments, M, A and B. M is the market portfolio, while A and B are individual stocks. The equilibrium mean vector =(15%20%25%)T, with the three entries corresponding to M,A and B. The prior covariance matrix for the three instruments are estimated at: =225104100104100104100104400104100104100104100104625104 Express the following views under Black-Litterman Model. Specifically, specify the matrix P and the corresponding vector . (i) "The market will rise by 25% ". (ii) "The market will rise by 12% ", "I'm bullish on Stock A", "I'm bearish on Stock B". (iii) "Stock A will underperform the market by 1%

All parts in this problem are under the setting of Black-Litterman model. Assume the risk-free rate is 0% under all parts. (a). Suppose there are three instruments, M, A and B. M is the market portfolio, while A and B are individual stocks. The equilibrium mean vector =(15%20%25%)T, with the three entries corresponding to M,A and B. The prior covariance matrix for the three instruments are estimated at: =225104100104100104100104400104100104100104100104625104 Express the following views under Black-Litterman Model. Specifically, specify the matrix P and the corresponding vector . (i) "The market will rise by 25% ". (ii) "The market will rise by 12% ", "I'm bullish on Stock A", "I'm bearish on Stock B". (iii) "Stock A will underperform the market by 1% Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Currency And Finance In Time Of War A Lecture

Authors: Francis Ysidro Edgeworth

1st Edition

1178449807, 9781178449808