Answered step by step

Verified Expert Solution

Question

1 Approved Answer

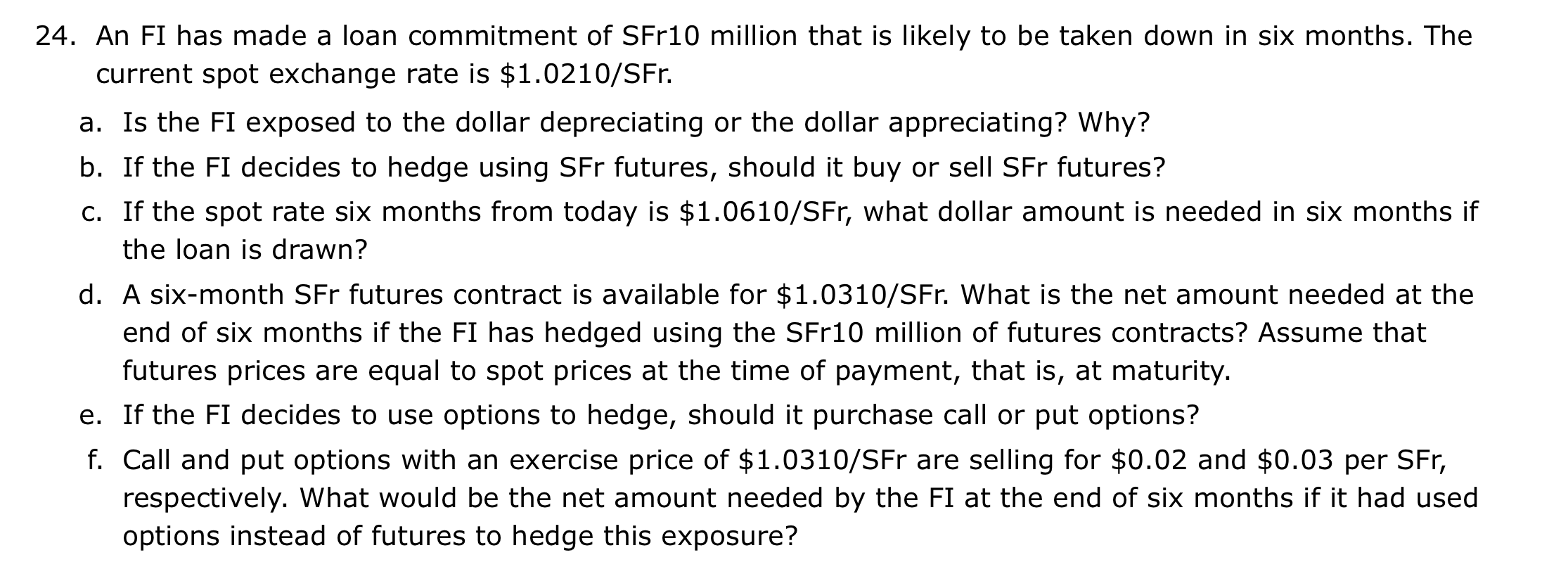

An FI has made a loan commitment of SFr 1 0 million that is likely to be taken down in six months. The current spot

An FI has made a loan commitment of SFr million that is likely to be taken down in six months. The

current spot exchange rate is $

a Is the FI exposed to the dollar depreciating or the dollar appreciating? Why?

b If the FI decides to hedge using SFr futures, should it buy or sell SFr futures?

c If the spot rate six months from today is $ what dollar amount is needed in six month if

the loan is drawn?

d A sixmonth SFr futures contract is available for $ SFr What is the net amount needed at the

end of six months if the FI has hedged using the SFr million of futures contracts? Assume that

futures prices are equal to spot prices at the time of payment, that is at maturity.

e If the FI decides to use options to hedge, should it purchase call or put options?

f Call and put options with an exercise price of $ are selling for $ and $ per

respectively. What would be the net amount needed by the FI at the end of six months if it had used

options instead of futures to hedge this exposure?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Overcoming Debt Achieving Financial Freedom

Authors: Cindy Zuniga-Sanchez

1st Edition

1119902320, 978-1119902324