Answered step by step

Verified Expert Solution

Question

1 Approved Answer

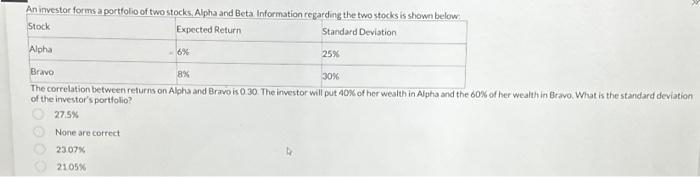

An investor forms a portfolio of two stocks, Alpha and Beta. Information regarding the two stocks is shown below: Stock Expected Return Standard Deviation Alpha

An investor forms a portfolio of two stocks, Alpha and Beta. Information regarding the two stocks is shown below: Stock Expected Return Standard Deviation Alpha 6% 000 Bravo 8% 30% The correlation between returns on Alpha and Bravo is 0.30. The investor will put 40% of her wealth in Alpha and the 60% of her wealth in Bravo. What is the standard deviation of the investor's portfolio? 27.5% None are correct 23.07% 21.05% 25% 4

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essentials of Investments

Authors: Zvi Bodie, Alex Kane, Alan Marcus

9th edition

78034698, 978-0077502287, 77502280, 978-0078034695