Question

An investor produces the efficient frontier and capital market line (CML) given in the figure below using two risk portfolios A and B and a

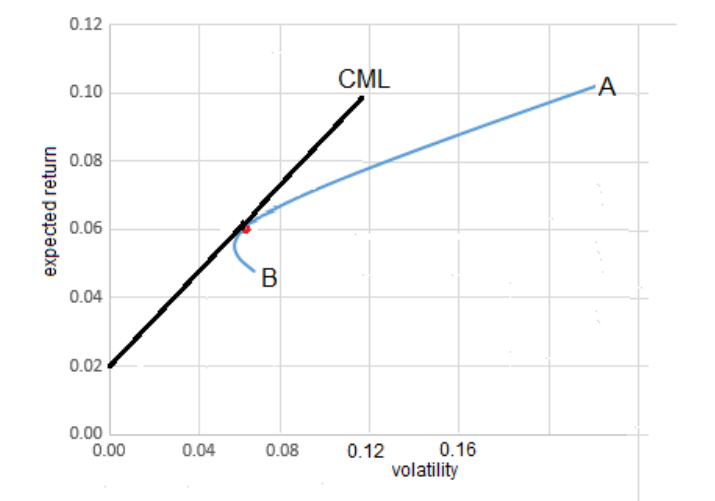

An investor produces the efficient frontier and capital market line (CML) given in the figure below using two risk portfolios A and B and a risk-free rate of 2%. The tangency portfolio has a volatility of 6.4% and an expected return of 6%.

a) Calculate the Sharpe ratio of the tangency portfolio. (5 marks)

b) What would be the expected return and volatility of a portfolio whose final allocations in the tangency portfolio and the risk-free asset given above are 40% and 60% respectively? (5 marks)

c) If borrowing at 2% is possible, how would one attain a portfolio that has 9% expected return using the tangency portfolio above? What weights would need to be chosen for the tangency portfolio and the risk-free asset to attain 9% overall expected return? (5 marks)

0.12 CML 0.10 A . 0.08 expected return 0.06 B 0.04 0.02 0.00 0.00 0.04 0.08 0.12 0.16 volatilityStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Renewable Energy Finance Powering The Future

Authors: Charles W. Donovan

1st Edition

178326778X, 9781783267781