Answered step by step

Verified Expert Solution

Question

1 Approved Answer

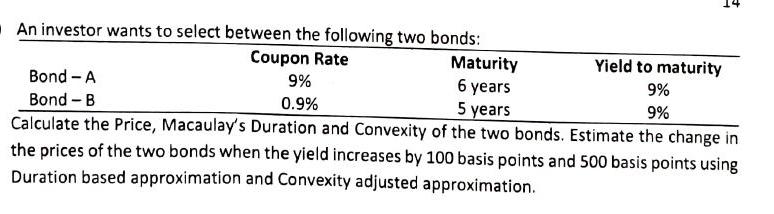

An investor wants to select between the following two honds. Calculate tne rrice, Macaulay's Duration and Convexity of the two bonds. Estimate the change in

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Mastering Cloud Auditing A Comprehensive Guide To Learn Cloud Auditing

Authors: Cybellium Ltd, Kris Hermans

1st Edition

B0CHL8DYC7, 979-8861283809