Question

An perfectly competitive industry consists of N firms, each one of which has a cost function given by: , where qi is the output of

An perfectly competitive industry consists of N firms, each one of which has a cost function given by: , where qi is the output of firm i in any given period. The per period market demand for this industry is given by P = 20 - 4Q.

A. What is the industry supply function?

B. What is the equilibrium market price and quantity?

C. What is the per period profit of each firm?

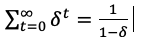

D. Suppose a N+1 firm can enter this industry but must pay an entry cost of 1. The firm will compare the present discounted value of its profits after entry with the entry cost. It will enter if the present discounted value of the profits exceeds the entry cost and stay out otherwise. If the firm's discount factor is ? = 0.9 and the firm expects no change in the demand and supply sides of this industry would it want to enter the industry if N=10? How about if N=20?

Assume that the entrant takes into consideration the effect that its entry will have on the market price. Also note:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Economics and Business Strategy

Authors: Michael R. baye

7th Edition

978-0073375960, 71267441, 73375969, 978-0071267441