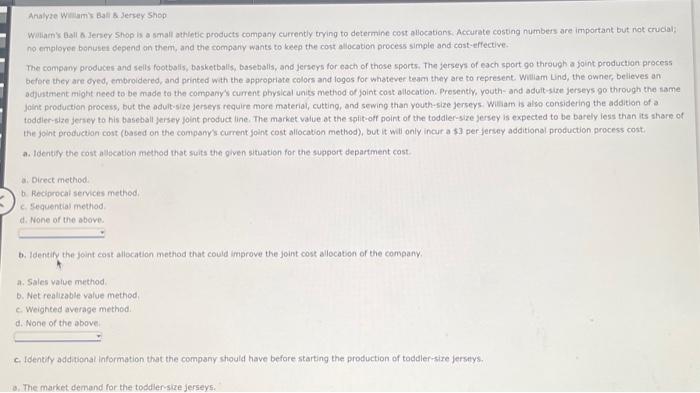

Analyze Whalamis bali o Jersey Shop Witarn' Ball a Jeney Shop is a small athletic products company currently trying to determine cost abocations: Acrurate costing numbers are important but not crucial: no employer bonuset depend on them, and the company wants to keep the cost allocation process simple and cost-effective. The company produces and sells footbolis, bssketballs, baseballs, and jerseys for each of those sports, The jerseys of each sport go through a joint production process before they are oyed, embroidered, and printed with the oppropriate colors and logos for whatever team they are to represent. Whillam Lind, the owner, believes an adjustment might need to be made to the company's current pbysical units method of joint cost allocation. Prosently, youth-and adult-size jerseys go through the same Joint production process; but the adult-size jerseys require more materiat, cutting, and sewing than youth-size jerseys: Wiliam is also considering the addition of a toddier-size jersey to his baseball jersey joint product line. The market value ot the spiti-off point of the toddier-size jersey is expected to be barely iess than its share of the joint production cost (based on the compsoy's current foint cost allocation method), but it will only incur a $3 per-jersey additional production process cost. a. Identify the cost allecation method that suits the given situation for the support department cost. a. Direct method. b. Reciprocal services methed. c. Sequential method. d. None of the above. b. Identify the joint cost allecation method that could improve the joint cost allocation of the company. a. Sales value method b. Net realizable value method, c. Weighied average method. d. None of the above. c. Identify additional information that the company should have before starting the production of toddler-sixe jersitys. Analyze Whalamis bali o Jersey Shop Witarn' Ball a Jeney Shop is a small athletic products company currently trying to determine cost abocations: Acrurate costing numbers are important but not crucial: no employer bonuset depend on them, and the company wants to keep the cost allocation process simple and cost-effective. The company produces and sells footbolis, bssketballs, baseballs, and jerseys for each of those sports, The jerseys of each sport go through a joint production process before they are oyed, embroidered, and printed with the oppropriate colors and logos for whatever team they are to represent. Whillam Lind, the owner, believes an adjustment might need to be made to the company's current pbysical units method of joint cost allocation. Prosently, youth-and adult-size jerseys go through the same Joint production process; but the adult-size jerseys require more materiat, cutting, and sewing than youth-size jerseys: Wiliam is also considering the addition of a toddier-size jersey to his baseball jersey joint product line. The market value ot the spiti-off point of the toddier-size jersey is expected to be barely iess than its share of the joint production cost (based on the compsoy's current foint cost allocation method), but it will only incur a $3 per-jersey additional production process cost. a. Identify the cost allecation method that suits the given situation for the support department cost. a. Direct method. b. Reciprocal services methed. c. Sequential method. d. None of the above. b. Identify the joint cost allecation method that could improve the joint cost allocation of the company. a. Sales value method b. Net realizable value method, c. Weighied average method. d. None of the above. c. Identify additional information that the company should have before starting the production of toddler-sixe jersitys