answer for question 1 and 2 pls

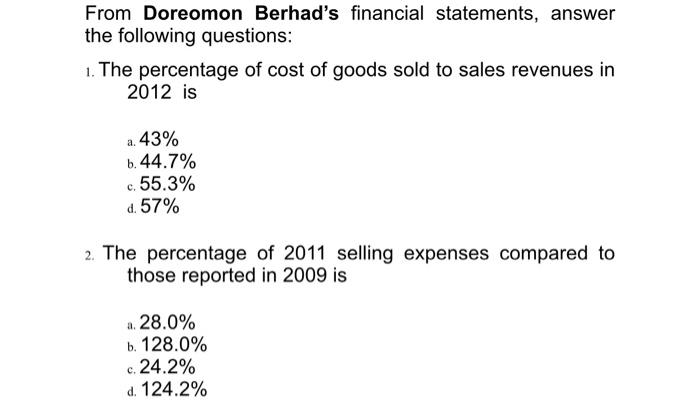

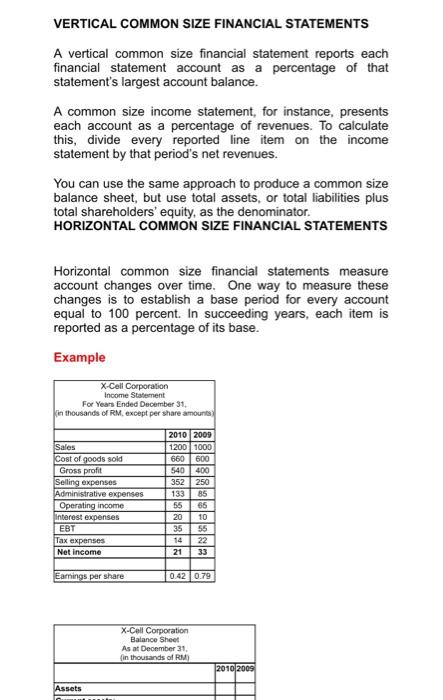

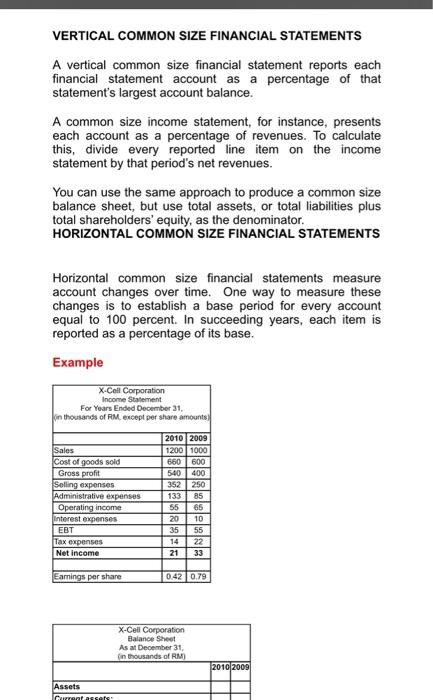

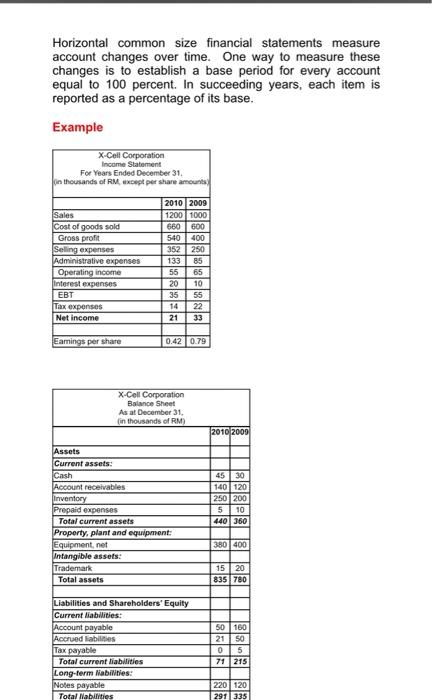

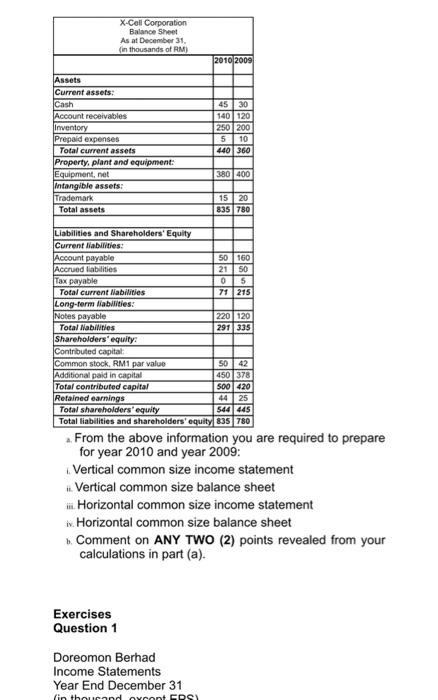

From Doreomon Berhad's financial statements, answer the following questions: 1. The percentage of cost of goods sold to sales revenues in 2012 is a. 43% b. 44.7% c. 55.3% d. 57% 2. The percentage of 2011 selling expenses compared to those reported in 2009 is a. 28.0% b. 128.0% c. 24.2% d. 124.2% Comparable financial statements simplify analysis, but dissimilar disclosures mix-up it. Benchmarking economic results is an important part of analysis, but financial statement variability complicates the task. Firms differ in size and entities changes over time. Standardizing financial disclosures solves the problem. This topic presents one of the technique for equating data sets over time and among companies. Basic Common-Size Financial Statement Considerations Common size financial statements report financial statement disclosures as a percentage of another account or as a proportion of their previous balance. You can restate the monetary value of cost of goods sold (COGS), for example, as a percentage (%) of the same period's revenues. Similarly, the current COGS can be recast as a \% of the previous year's COGS. Analyzing the % term, instead of the dollar amounts, helps analysts evaluate financial statements, compare firms, and benchmark over time. You would gain little knowledge by comparing the absolute dollar amount of net income earned a decade ago with the past year's profit. The amount of revenues generating those two income streams was, in all likelihood, quite different. Comparing earnings as a % of revenues for those two years produces a more meaningful within company evaluation. The argument also applies to comparisons among companies. This topic will demonstrates how to common size financial statements in two ways. We demonstrate vertical and horizontal common sizing using eSTUFF's income statement and balance sheet accounts. We then conclude by examining the mathematical parts of vertical and horizontal common size statements. VERTICAL COMMON SIZE FINANCIAL STATEMENTS VERTICAL COMMON SIZE FINANCIAL STATEMENTS A vertical common size financial statement reports each financial statement account as a percentage of that statement's largest account balance. A common size income statement, for instance, presents each account as a percentage of revenues. To calculate this, divide every reported line item on the income statement by that period's net revenues. You can use the same approach to produce a common size balance sheet, but use total assets, or total liabilities plus total shareholders' equity, as the denominator. HORIZONTAL COMMON SIZE FINANCIAL STATEMENTS Horizontal common size financial statements measure account changes over time. One way to measure these changes is to establish a base period for every account equal to 100 percent. In succeeding years, each item is reported as a percentage of its base. Example VERTICAL COMMON SIZE FINANCIAL STATEMENTS A vertical common size financial statement reports each financial statement account as a percentage of that statement's largest account balance. A common size income statement, for instance, presents each account as a percentage of revenues. To calculate this, divide every reported line item on the income statement by that period's net revenues. You can use the same approach to produce a common size balance sheet, but use total assets, or total liabilities plus total shareholders' equity, as the denominator. HORIZONTAL COMMON SIZE FINANCIAL STATEMENTS Horizontal common size financial statements measure account changes over time. One way to measure these changes is to establish a base period for every account equal to 100 percent. In succeeding years, each item is reported as a percentage of its base. Example Horizontal common size financial statements measure account changes over time. One way to measure these changes is to establish a base period for every account equal to 100 percent. In succeeding years, each item is reported as a percentage of its base. Example a. From the above information you are required to prepare for year 2010 and year 2009 : i. Vertical common size income statement ii Vertical common size balance sheet iii. Horizontal common size income statement iv. Horizontal common size balance sheet b. Comment on ANY TWO (2) points revealed from your calculations in part (a). From Doreomon Berhad's financial statements, answer the following questions: 1. The percentage of cost of goods sold to sales revenues in 2012 is a. 43% b. 44.7% c. 55.3% d. 57% 2. The percentage of 2011 selling expenses compared to those reported in 2009 is a. 28.0% b. 128.0% c. 24.2% d. 124.2% Comparable financial statements simplify analysis, but dissimilar disclosures mix-up it. Benchmarking economic results is an important part of analysis, but financial statement variability complicates the task. Firms differ in size and entities changes over time. Standardizing financial disclosures solves the problem. This topic presents one of the technique for equating data sets over time and among companies. Basic Common-Size Financial Statement Considerations Common size financial statements report financial statement disclosures as a percentage of another account or as a proportion of their previous balance. You can restate the monetary value of cost of goods sold (COGS), for example, as a percentage (%) of the same period's revenues. Similarly, the current COGS can be recast as a \% of the previous year's COGS. Analyzing the % term, instead of the dollar amounts, helps analysts evaluate financial statements, compare firms, and benchmark over time. You would gain little knowledge by comparing the absolute dollar amount of net income earned a decade ago with the past year's profit. The amount of revenues generating those two income streams was, in all likelihood, quite different. Comparing earnings as a % of revenues for those two years produces a more meaningful within company evaluation. The argument also applies to comparisons among companies. This topic will demonstrates how to common size financial statements in two ways. We demonstrate vertical and horizontal common sizing using eSTUFF's income statement and balance sheet accounts. We then conclude by examining the mathematical parts of vertical and horizontal common size statements. VERTICAL COMMON SIZE FINANCIAL STATEMENTS VERTICAL COMMON SIZE FINANCIAL STATEMENTS A vertical common size financial statement reports each financial statement account as a percentage of that statement's largest account balance. A common size income statement, for instance, presents each account as a percentage of revenues. To calculate this, divide every reported line item on the income statement by that period's net revenues. You can use the same approach to produce a common size balance sheet, but use total assets, or total liabilities plus total shareholders' equity, as the denominator. HORIZONTAL COMMON SIZE FINANCIAL STATEMENTS Horizontal common size financial statements measure account changes over time. One way to measure these changes is to establish a base period for every account equal to 100 percent. In succeeding years, each item is reported as a percentage of its base. Example VERTICAL COMMON SIZE FINANCIAL STATEMENTS A vertical common size financial statement reports each financial statement account as a percentage of that statement's largest account balance. A common size income statement, for instance, presents each account as a percentage of revenues. To calculate this, divide every reported line item on the income statement by that period's net revenues. You can use the same approach to produce a common size balance sheet, but use total assets, or total liabilities plus total shareholders' equity, as the denominator. HORIZONTAL COMMON SIZE FINANCIAL STATEMENTS Horizontal common size financial statements measure account changes over time. One way to measure these changes is to establish a base period for every account equal to 100 percent. In succeeding years, each item is reported as a percentage of its base. Example Horizontal common size financial statements measure account changes over time. One way to measure these changes is to establish a base period for every account equal to 100 percent. In succeeding years, each item is reported as a percentage of its base. Example a. From the above information you are required to prepare for year 2010 and year 2009 : i. Vertical common size income statement ii Vertical common size balance sheet iii. Horizontal common size income statement iv. Horizontal common size balance sheet b. Comment on ANY TWO (2) points revealed from your calculations in part (a)