Answer with solution and explanation

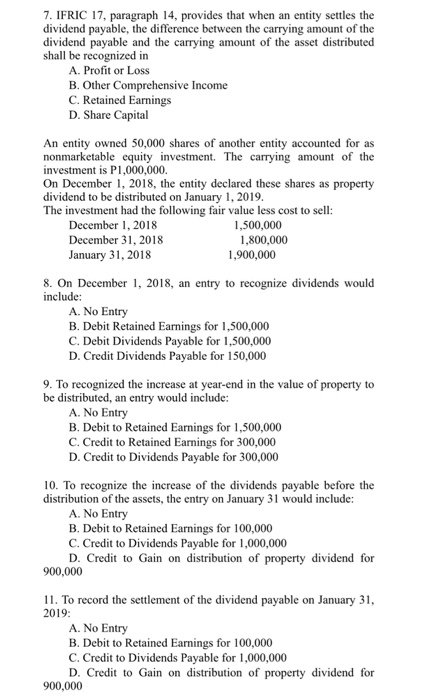

7. IFRIC 17, paragraph 14, provides that when an entity settles the dividend payable, the difference between the carrying amount of the dividend payable and the carrying amount of the asset distributed shall be recognized in A. Profit or Loss B. Other Comprehensive Income C. Retained Earnings D. Share Capital An entity owned 50,000 shares of another entity accounted for as nonmarketable equity investment. The carrying amount of the investment is P1,000,000. On December 1, 2018, the entity declared these shares as property dividend to be distributed on January 1, 2019 The investment had the following fair value less cost to sell: December 1, 2018 December 31, 2018 January 31, 2018 1,500,000 1,800,000 1,900,000 8. On December 1, 2018, an entry to recognize dividends would include: A. No Entry B. Debit Retained Earnings for 1,500,000 C. Debit Dividends Payable for 1,500,000 D. Credit Dividends Payable for 150,000 9. To recognized the increase at year-end in the value of property to be distributed, an entry would include: A. No Entry B. Debit to Retained Earnings for 1,500,000 C. Credit to Retained Earnings for 300,000 D. Credit to Dividends Payable for 300,000 10. To recognize the increase of the dividends payable before the distribution of the assets, the entry on January 31 would include: A. No Entry B. Debit to Retained Earnings for 100,000 C. Credit to Dividends Payable for 1,000,000 D. Credit to Gain on distribution of property dividend for 900,000 11. To record the settlement of the dividend payable on January 31 2019: A. No Entry B. Debit to Retained Earnings for 100,000 C. Credit to Dividends Payable for 1,000,000 D. Credit to Gain on distribution of property dividend for 900,000 7. IFRIC 17, paragraph 14, provides that when an entity settles the dividend payable, the difference between the carrying amount of the dividend payable and the carrying amount of the asset distributed shall be recognized in A. Profit or Loss B. Other Comprehensive Income C. Retained Earnings D. Share Capital An entity owned 50,000 shares of another entity accounted for as nonmarketable equity investment. The carrying amount of the investment is P1,000,000. On December 1, 2018, the entity declared these shares as property dividend to be distributed on January 1, 2019 The investment had the following fair value less cost to sell: December 1, 2018 December 31, 2018 January 31, 2018 1,500,000 1,800,000 1,900,000 8. On December 1, 2018, an entry to recognize dividends would include: A. No Entry B. Debit Retained Earnings for 1,500,000 C. Debit Dividends Payable for 1,500,000 D. Credit Dividends Payable for 150,000 9. To recognized the increase at year-end in the value of property to be distributed, an entry would include: A. No Entry B. Debit to Retained Earnings for 1,500,000 C. Credit to Retained Earnings for 300,000 D. Credit to Dividends Payable for 300,000 10. To recognize the increase of the dividends payable before the distribution of the assets, the entry on January 31 would include: A. No Entry B. Debit to Retained Earnings for 100,000 C. Credit to Dividends Payable for 1,000,000 D. Credit to Gain on distribution of property dividend for 900,000 11. To record the settlement of the dividend payable on January 31 2019: A. No Entry B. Debit to Retained Earnings for 100,000 C. Credit to Dividends Payable for 1,000,000 D. Credit to Gain on distribution of property dividend for 900,000