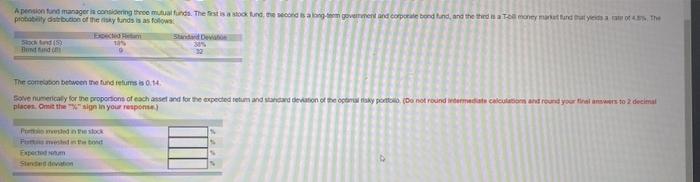

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a Tell money market fund that yields a rate of 4. The probability distribution of the risky funds is as follows Stock and (5) Bund fand Expected Rea 10% Standard Deviation 30% The correlation between the fund retums is 0.14. Solve numerically for the proportions of each asset and for the expected retum and standard deviation of the optimal risky portfolio, (Do not round intermediate calculations and round your final answers to 2 decimal places. Omit the "%" sign in your response) Posted in Tok Fu meshed in the bond Expected m Stended deviation 4

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To solve for the optimal portfolio we will apply the principles of portfolio optimization using the given data expected returns standard deviations an...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Gabriel Hawawini, Claude Viallet

4th edition

9781133169949, 538751347, 978-0538751346