Question

Arbitrage problem - The mechanics of exchange rate arithmetic, though fundamentally simple, can be confusing for those not using it on a regular basis. The

Arbitrage problem - The mechanics of exchange rate arithmetic, though fundamentally simple, can be confusing for those not using it on a regular basis. The questions below are designed to provide practice in the more common manipulations. They are of low to moderate difficulty with the easiest problems occurring first. Exhibits 1-3, along with general background information provided in this note, are sufficient to solve the problem

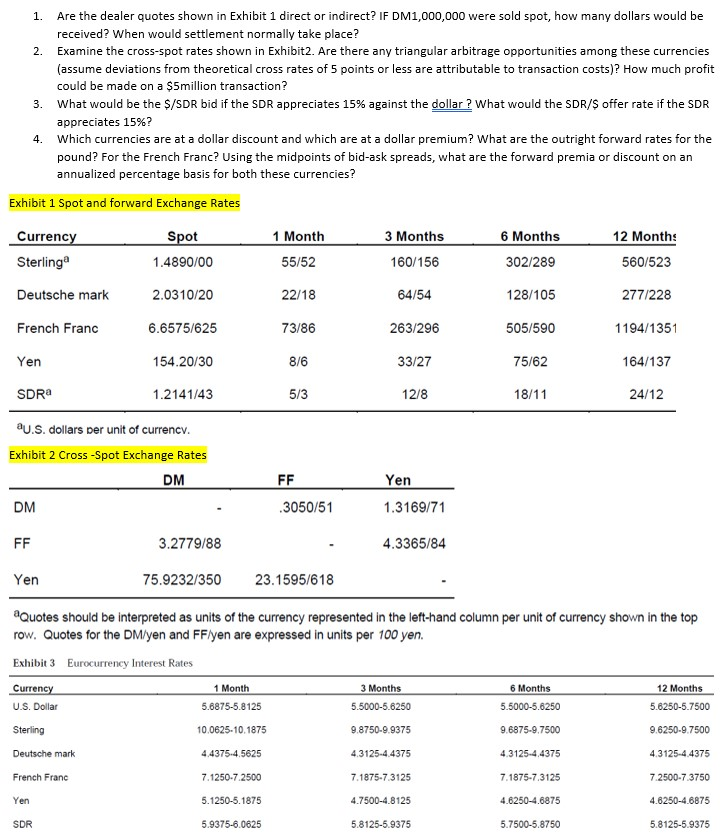

1. Are the dealer quotes shown in Exhibit 1 direct or indirect? If DM1,000,000 were sold spot how many dollars would be received? When would settlement normally take place? The mechanics of exchange rate arithmetic, though fundamentally simple, can be confusing for those not using it on a regular basis. The questions below are designed to provide practice in the more common manipulations. They are of low to moderate difficulty with the easiest problems occurring first. Exhibits 1-3, along with general background information provided in this note, are sufficient to solve the problem

2. Examine the cross-spot rates shown in Exhibit 2. Are there any triangular arbitrage opportunities among these currencies (assume deviations from theoretical cross rates of 5 points or less are attributable to transaction costs)? How much profit could be made on a $5 million transaction?

1. Are the dealer quotes shown in Exhibit 1 direct or indirect? IF DM1,000,000 were sold spot, how many dollars would be received? When would settlement normally take place? 2. Examine the cross-spot rates shown in Exhibit2. Are there any triangular arbitrage opportunities among these currencies (assume deviations from theoretical cross rates of 5 points or less are attributable to transaction costs)? How much profit could be made on a $5million transaction? 3. What would be the $/SDR bid if the SDR appreciates 15% against the dollar? What would the SDR/S offer rate if the SDR appreciates 15%? Which currencies are at a dollar discount and which are at a dollar premium? What are the outright forward rates for the pound? For the French Franc? Using the midpoints of bid-ask spreads, what are the forward premia or discount on an annualized percentage basis for both these currencies? Exhibit 1 Spot and forward Exchange Rates 4. Currency Sterling Spot 1.4890/00 1 Month 55/52 3 Months 160/156 6 Months 302/289 12 Month: 560/523 Deutsche mark 2.0310/20 22/18 64/54 128/105 277/228 French Franc 6.6575/625 73/86 263/296 505/590 1194/1351 Yen 154.20/30 8/6 33/27 75/62 164/137 SDR 1.2141/43 5/3 12/8 18/11 24/12 au.S. dollars per unit of currency. Exhibit 2 Cross-Spot Exchange Rates DM FF Yen 1.3169/71 DM .3050/51 FF 3.2779/88 4.3365/84 Yen 75.9232/350 23.1595/618 6 Months aQuotes should be interpreted as units of the currency represented in the left-hand column per unit of currency shown in the top row. Quotes for the DM/yen and FF/yen are expressed in units per 100 yen. Exhibit 3 Eurocurrency Interest Rates Currency 1 Month 3 Months 5.6875-5.8125 5.5000-5.6250 5.5000-5.6250 Sterling 10.0625.10.1875 9.8750-9.9375 9.6875-9.7500 Deutsche mark 4.3125-4.4375 7.1875-7.3125 12 Months 5.6250-5.7500 U.S. Dollar 9.6250-9.7500 4.4375.4.5625 4.3125-4,4375 4.3125-4.4375 French Franc 7.1250-7.2500 7.1875-7.3125 7.2500-7.3750 Yen 5.1250-5.1875 4.7500-4.8125 4.6250-4.6875 4.6250-4.6875 SDR 5.9375-6.0625 5.8125-5.9375 5.7500-5.8750 5.8125-5.9375 1. Are the dealer quotes shown in Exhibit 1 direct or indirect? IF DM1,000,000 were sold spot, how many dollars would be received? When would settlement normally take place? 2. Examine the cross-spot rates shown in Exhibit2. Are there any triangular arbitrage opportunities among these currencies (assume deviations from theoretical cross rates of 5 points or less are attributable to transaction costs)? How much profit could be made on a $5million transaction? 3. What would be the $/SDR bid if the SDR appreciates 15% against the dollar? What would the SDR/S offer rate if the SDR appreciates 15%? Which currencies are at a dollar discount and which are at a dollar premium? What are the outright forward rates for the pound? For the French Franc? Using the midpoints of bid-ask spreads, what are the forward premia or discount on an annualized percentage basis for both these currencies? Exhibit 1 Spot and forward Exchange Rates 4. Currency Sterling Spot 1.4890/00 1 Month 55/52 3 Months 160/156 6 Months 302/289 12 Month: 560/523 Deutsche mark 2.0310/20 22/18 64/54 128/105 277/228 French Franc 6.6575/625 73/86 263/296 505/590 1194/1351 Yen 154.20/30 8/6 33/27 75/62 164/137 SDR 1.2141/43 5/3 12/8 18/11 24/12 au.S. dollars per unit of currency. Exhibit 2 Cross-Spot Exchange Rates DM FF Yen 1.3169/71 DM .3050/51 FF 3.2779/88 4.3365/84 Yen 75.9232/350 23.1595/618 6 Months aQuotes should be interpreted as units of the currency represented in the left-hand column per unit of currency shown in the top row. Quotes for the DM/yen and FF/yen are expressed in units per 100 yen. Exhibit 3 Eurocurrency Interest Rates Currency 1 Month 3 Months 5.6875-5.8125 5.5000-5.6250 5.5000-5.6250 Sterling 10.0625.10.1875 9.8750-9.9375 9.6875-9.7500 Deutsche mark 4.3125-4.4375 7.1875-7.3125 12 Months 5.6250-5.7500 U.S. Dollar 9.6250-9.7500 4.4375.4.5625 4.3125-4,4375 4.3125-4.4375 French Franc 7.1250-7.2500 7.1875-7.3125 7.2500-7.3750 Yen 5.1250-5.1875 4.7500-4.8125 4.6250-4.6875 4.6250-4.6875 SDR 5.9375-6.0625 5.8125-5.9375 5.7500-5.8750 5.8125-5.9375

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Loose Leaf For Financial Accounting Fundamentals

Authors: John Wild, Ken Shaw, Barbara Chiappetta

6th Edition

1260151980, 978-1260151985