Answered step by step

Verified Expert Solution

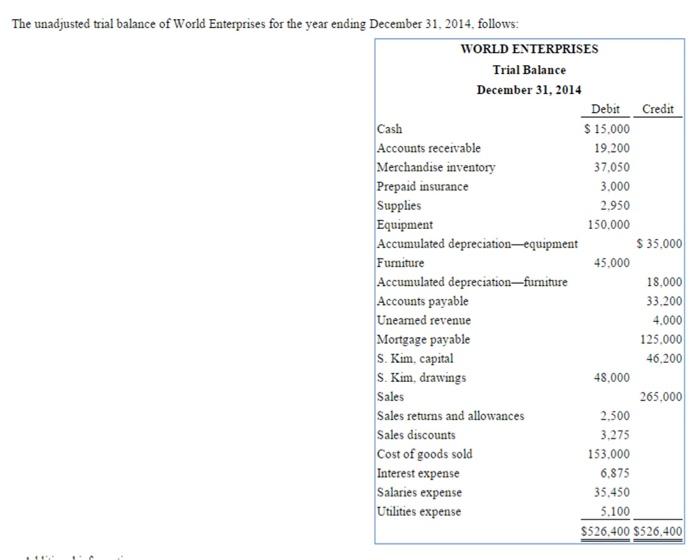

Question

1 Approved Answer

ASAP Additional information: There is $750 of supplies on hand on December 31, 2014. 2. The one-year insurance policy was purchased on March 1, 2014.

ASAP Additional information:

There is $750 of supplies on hand on December 31, 2014.

2. The one-year insurance policy was purchased on March 1, 2014.

3. Depreciation expense for the year is $10,000 for the equipment and $4,500 for the furniture.

4. Accrued interest expense at December 31, 2014, is $675.

5. Uneamed revenue of $975 is still uneamed at December 31, 2014. On the sales that were earned, cost of goods sold was $1,750.

6. A physical count of merchandise inventory indicates $32,750 on hand on December 31, 2014.

7. Of the mortgage payable, $8,500 is to be paid in 2015.

S. Seok Kim invested $5,000 cash in the business on July 19,2014.

9. Last year, the company had a gross profit margin of 35%, and profit margin of 10%.

Instructions

(a) Prepare the adjusting journal entries assuming they are prepared annually

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting

Authors: Donald E. Kieso, Jerry J. Weygandt, And Terry D. Warfield

13th Edition

9780470374948, 470423684, 470374942, 978-0470423684