Ash & John: Accounting for Business Decisions During COVID-19 Ash & John is a Brisbane-based sole-trader that operates at a retail shopfront. The store specialises

Ash & John: Accounting for Business Decisions During COVID-19

Ash & John is a Brisbane-based sole-trader that operates at a retail shopfront. The store specialises in selling tennis racquets but also offers tennis racquet stringing services. The owner

of the Ash & John, Mrs Stosur, does not manage the store herself, instead, a store manager, Nick K, was hired to manage the day-to-day business. Ash & John’s sales typically peak in January when the Australian Open tennis tournament takes place in mid-January and attracts new following to the sport. However, in 2021, the store’s January sales was uncharacteristically low, in fact, the business had suffered a severe decline in sales for months as a direct result of COVID-19 restrictions. The pandemic prohibited sports activities and as a result reduced in-store shopping.

Early January 2021 - Business in Recovery

Despite the financial difficulties in 2020, at the start of 2021, Nick was confident that the sales at the store would start to grow as life was slowly and steadily getting back to normal in Queensland thanks to the state government’s effective disease management. This optimistic view was reinforced by the arrival of a large order from the local tennis club, Hewitt Tennis, in early January. On 4 January, Hewitt Tennis ordered racquets to be delivered to the club on 18 January. The goods were priced for sale at $5,500 and were acquired from the supplier at a discounted price of $2,130. Hewitt Tennis paid $3,500 upon the delivery of goods and made the remaining payment on 5 February. In preparation of the order as well as the anticipated sales increase, Nick ordered premium tennis racquets with the latest design from the major brands on 4 January. There were no additional purchases of lower-priced racquets as these products were in abundance in the inventory. One batch of Babolat and Head racquets with a total cost of $7,200 arrived on 5 January, the payments were due in three instalments of equal amounts over the next 60 days, the first instalment was made to the supplier on 24 January, the other two payments were made later in February. A separate batch of Wilson racquets were delivered to the store with an invoice of $1,900 on 7 January. Ash & John paid for this purchase in cash in full. As cash balance became critically low after the payment for Wilson racquets, Nick took out a short-term loan of $3,000 under the name of Ash & John on 8 January to maintain a healthy cash position. In addition to this large order, Ash & John also earn a contract with Hewitt Tennis to offer on-site racquet stringing service at the club’s biggest annual event, the Lleyton Cup, in February. $1,200 cash were received for the contracted service when the contract was signed on 6 January. In preparation of this service provision, Nick made the business decision to increase Ash & John’s service capacity by acquiring a second-hand stringing machine in good condition from one of the competing sports stores that recently filed bankruptcy. Nick agreed to a bargain price of $800 for the machine after much negotiation on 9 January before picking up the machine on 15 January and paying in cash in full. Other sales in early January include a $680 cash sale on 3 January of goods that cost $440, and a $950 credit sale on 11 January of goods that cost $680. In terms of service provision, Nick sold a prepaid package of 10 standard stringing services for $600 cash on 10 January, the customer used up two services on day. The package is valid for use within 180 days from the day of purchase. During this period, Ash & John also provided a large volume of stringing service to Queensland Tennis Centre. This service was booked and prepaid for in December last year. The discount bulk charge averaged $50 per service. On 31 January, the provision of a total of 133 services was accounted for.

Mid to Late January 2021 - Another Period of Struggle

Just as the sales began to increase, the reported cases of UK strain of COVID-19 sent the greater Brisbane area into a three-day lock down between 11 and 14 January 2021. The lock down along with the requirement of mandatory use of facial masks in certain public indoor spaces between 11 and 22 January caused the store sales to plummet. Very few customers visited the store since 11 January, and Nick only managed to make two small sales during this time: a credit sale of $80 goods that cost $50 on 19 January and another credit sale of $130 at cost $90 on 26 January. There was no purchase of stringing services in this period. The most difficult aspect of operating a physical store in this period is the fact that many expenses were unavoidable despite of the low volume of business activities at the store. The weekly rent for the shopfront is $350, payable every four weeks in advance. The first rental payment of 2021 was made on 4 January to cover the four-week period starting 8 January. The staffing costs were also substantial. Nick was paid $40,560 per annum, averaged $780 per week or $130 per day (6 days of work in a week; Wednesdays off). Nick received fortnightly salary payments on 14 and 28 January to cover the salary period from 1 to 28 January. The store’s only sales assistant Bernard

T. held a casual position and was paid at $25 per hour with a guaranteed minimum work allocation of 10 hours per week. Bernard received the minimum amount of his fortnightly wage payment $500 on 14 January with the sad news that Ash & John was no longer in the position to continue his employment. There was also depreciation and insurance premium. Both depreciation andstore insurance expenses are recognised on a monthly basis at the month end. Ash & John last paid the insurance premium $7,300 on 31 December to cover any loss of inventory and cases of staff injuries for the next 365 days. In terms of utility, the next electricity bill would not arrive before February.

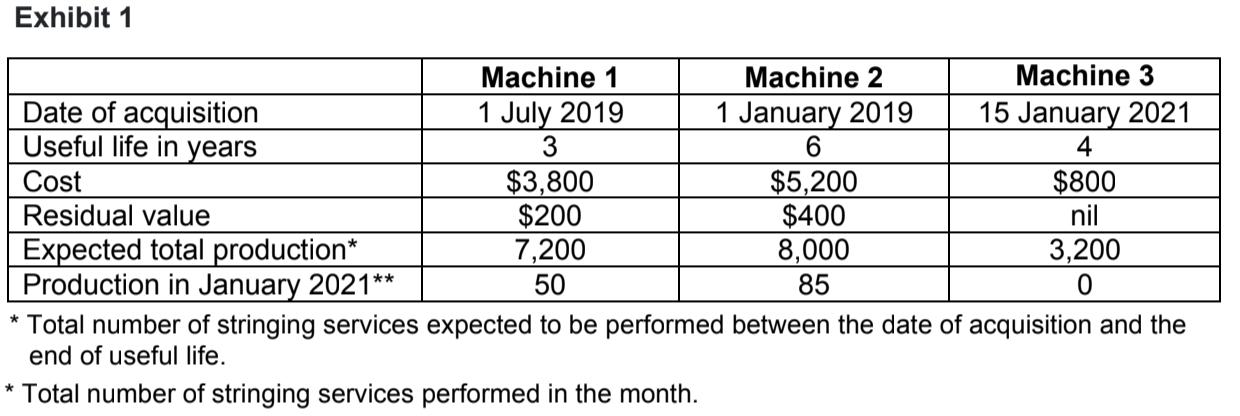

Depreciation of Machines & Vehicle

As at 31 January 2021, Ash & John had three stringing machines. Details of these assets are

presented in Exhibit 1 below

The demand of stringing services declined significantly since the outbreak of COVID-19, as a result, Ash & John was considering the following options: (1) changing the depreciation method

regarding stringing machines from the straight-line method to the unit-of-production method, or (2) making no change to the depreciation method but re-evaluating the remaining useful life of

each machine. Ash & John also owns a delivery van that is used to deliver shipment and transport the stringing machines to customer sites for on-site service provision. The van was given to the business by Mrs Stosur on 1 July 2018 with an estimated useful life of 10 years and a residual value of $9,000. Depreciation of this vehicle is recognised using the straight-line depreciation method.

Potential Business Diversification

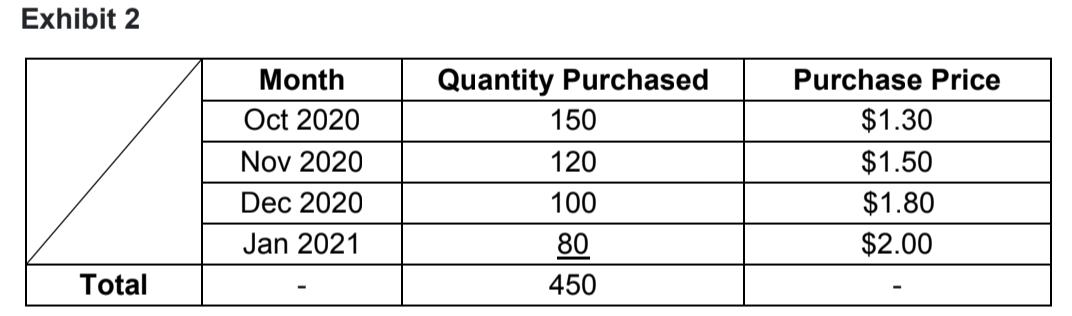

In August 2020, Mrs Stosur first expressed concern over the viability of her business after the business made a loss in the third consecutive month. Mrs Stosur asked Nick to help seek opportunities to diversify the business’s income. Nick quickly thought of the idea of selling used tennis balls. Nick is a tennis lover and plays club tennis at Hewitt Centre. He became aware that the club has a policy of disposing of used tennis balls after holding competitive events like the Lleyton Cup. Many of the disposed balls were in good condition and could have been readily used for general practice or casual playing at the club. Nick contacted the management at Hewitt Tennis in September 2020 and was successful in reaching an agreement with the club for the supply of used tennis balls. However, Mrs Stosur was not fully confident of this venture and decided to acquire the used tennis balls as her personal asset first. The store started to trial the sale of the used balls in October 2020; all transactions concerning the used tennis balls were regarded as Mrs Stosur’s personal transactions. The quantities of the monthly purchases of used tennis balls are detailed in Exhibit 2 below.

As the sales of tennis balls were not part of store’s official operation, Nick did not keep the record of cost of sales of these transactions but only the quantity of used balls sold. From 1 October

2020 to 31 January 2021, 380 used balls were sold at the price $2.40 each.

Changing Customer Behaviour At Ash & John,

customers who spend more than $150 in a single transaction may elect to purchase on credit, payable in 60 days. Despite the option, most sales at Ash & John were cash transactions prior to March 2020. However, since the outbreak of COVID-19, more and more customers have opted for credit purchases. This change in customer’s purchasing behaviour had added to the financial difficulties of the business, and Mr Stosur and Nick worried that Ash & John

would report a loss for the ninth consecutive month in January 2021.

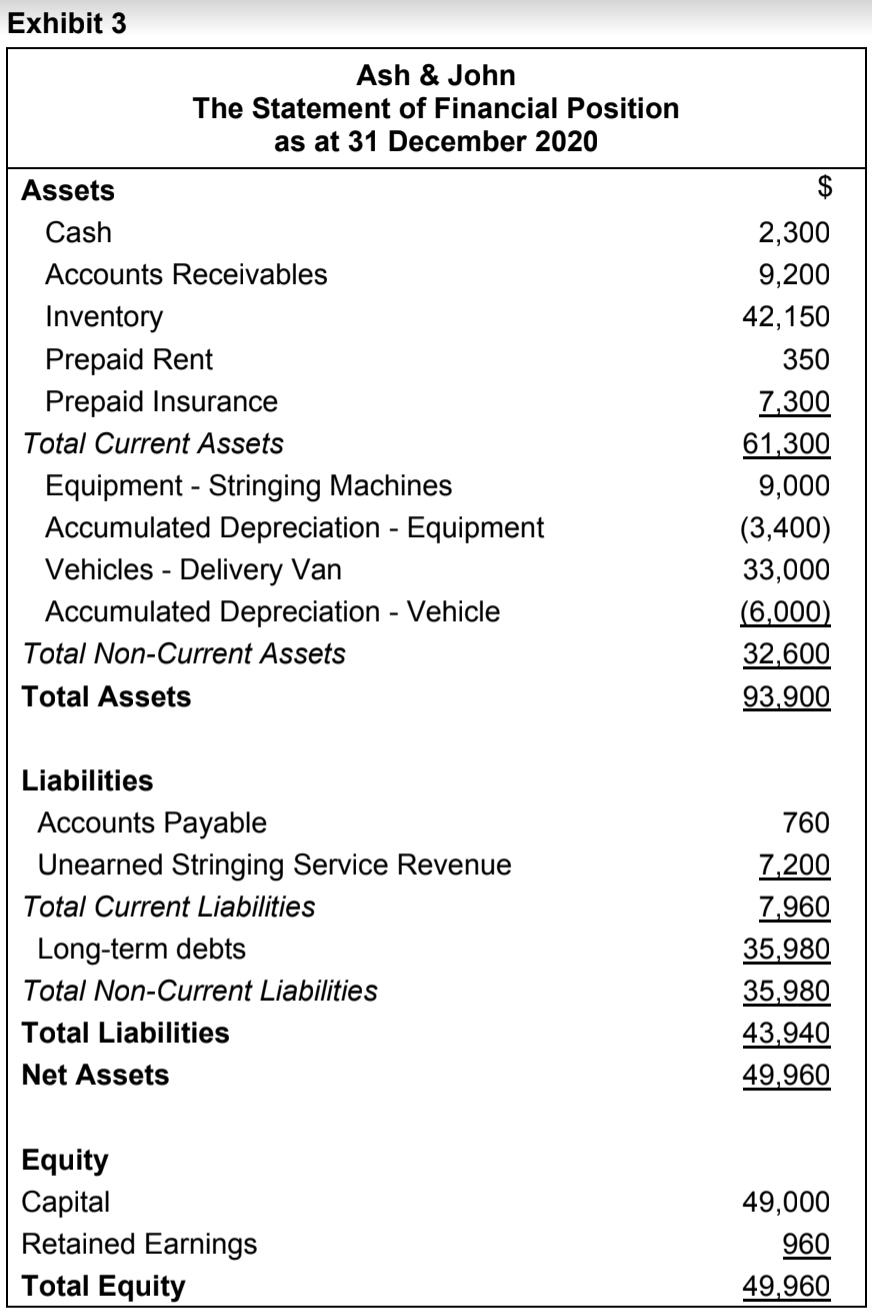

Ash & John’s Statement of Financial Position as at 31 December 2020

Question:

The case states that “The demand of stringing services declined significantly since the outbreak of COVID-19, as a result, Ash & John was considering the following options: (1) making no change to the depreciation method but re-evaluating the remaining useful life of each machine, or (2) changing the depreciation method regarding stringing machines from the straight-line method to the unit-of-production method.”

1 Discuss how may Option (1) be more appropriate than the original practice (i.e. to recognise depreciation using the straight-line method based on the information in Exhibit 1).

2. Discuss how may Option (2) be more appropriate than both the original practice (i.e. to recognise depreciation using the straight-line method based on the information in Exhibit 1) and Option (1) given the circumstances regarding the business. Cite specific information in the case to support your discussion where appropriate.

3. Would Ash & John report less depreciation expense for machine 2 in January 2021 if depreciation were always accounted for using the Diminishing-Balance Method since the start of the asset’s useful life? Include the patterns of cost allocation in your discussion.

Exhibit 1 Date of acquisition Useful life in years Cost Residual value Expected total production* Production in January 2021** Machine 1 1 July 2019 3 $3,800 $200 7,200 50 Machine 2 1 January 2019 6 $5,200 $400 8,000 85 Machine 3 15 January 2021 4 $800 nil 3,200 0 * Total number of stringing services expected to be performed between the date of acquisition and the end of useful life. * Total number of stringing services performed in the month. Exhibit 2 Total Month Oct 2020 Nov 2020 Dec 2020 Jan 2021 Quantity Purchased 150 120 100 80 450 Purchase Price $1.30 $1.50 $1.80 $2.00 Exhibit 3 Assets Cash Ash & John The Statement of Financial Position as at 31 December 2020 Accounts Receivables Inventory Prepaid Rent Prepaid Insurance Total Current Assets Equipment - Stringing Machines Accumulated Depreciation - Equipment Vehicles Delivery Van Accumulated Depreciation - Vehicle Total Non-Current Assets Total Assets Liabilities Accounts Payable Unearned Stringing Service Revenue Total Current Liabilities Long-term debts Total Non-Current Liabilities Total Liabilities Net Assets Equity Capital Retained Earnings Total Equity 2,300 9,200 42,150 350 7,300 61,300 9,000 (3,400) 33,000 (6,000) 32,600 93,900 760 7,200 7,960 35,980 35,980 43,940 49,960 49,000 960 49,960

Step by Step Solution

3.33 Rating (147 Votes )

There are 3 Steps involved in it

Step: 1

We shall start by finding the depreciation of the machines and the van Van uses straight line depreciation Cost33000 Depreciation330009000102400 The d...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Donald E. Kieso, Jerry J. Weygandt, And Terry D. Warfield

13th Edition

9780470374948, 470423684, 470374942, 978-0470423684