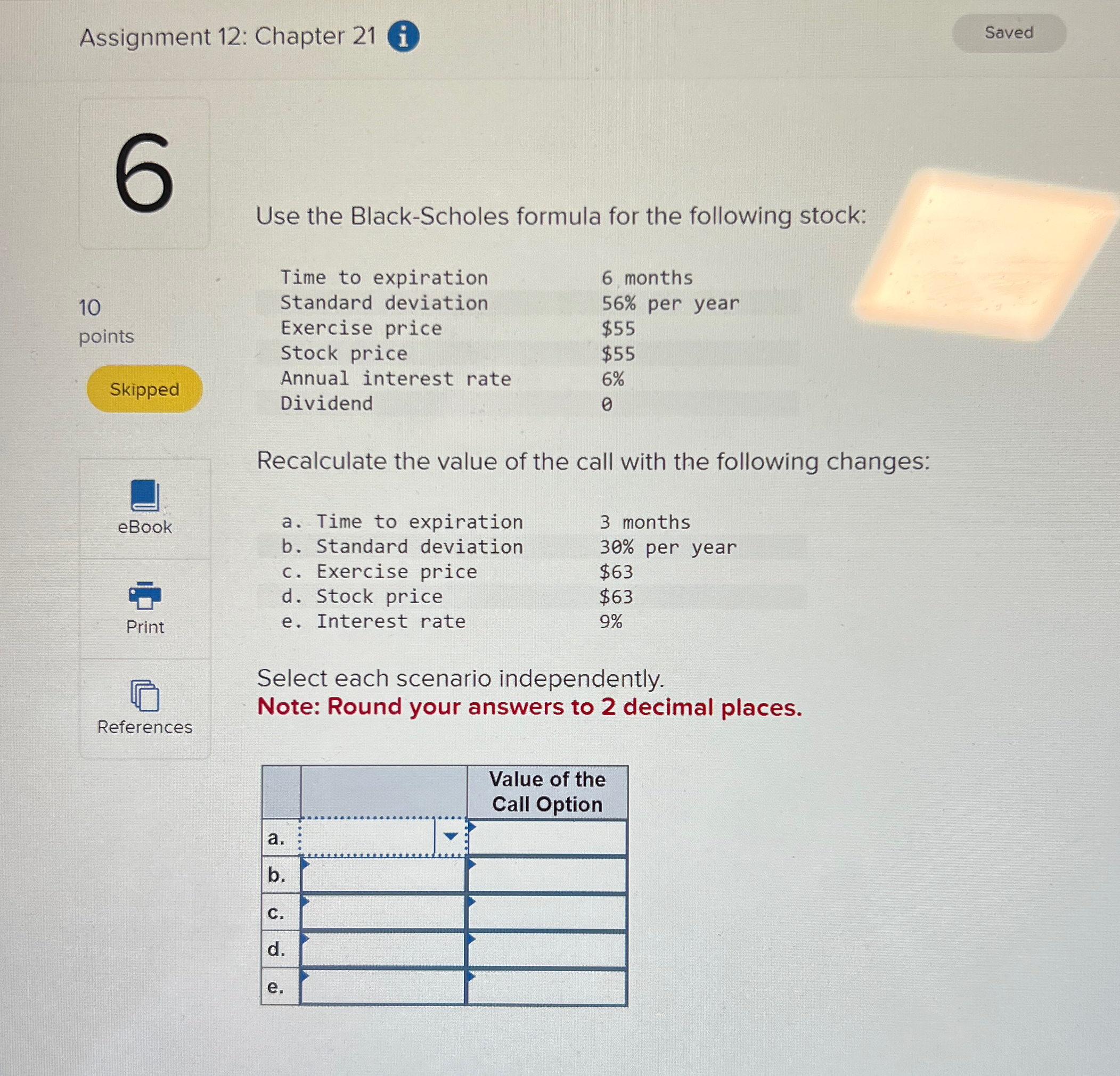

Question: Assignment 1 2 : Chapter 2 1 0 1 0 points Skipped eBook Print References Use the Black - Scholes formula for the following stock:

Assignment : Chapter

points

Skipped

eBook

Print

References

Use the BlackScholes formula for the following stock:

tableTime to expiration, monthsStandard deviation, per yearExercise price,$

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock