Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Assignment Questions: 1. What are the main issues facing John Smith? 2. What are the alternatives available for accounting, inventory, and advertising? How could

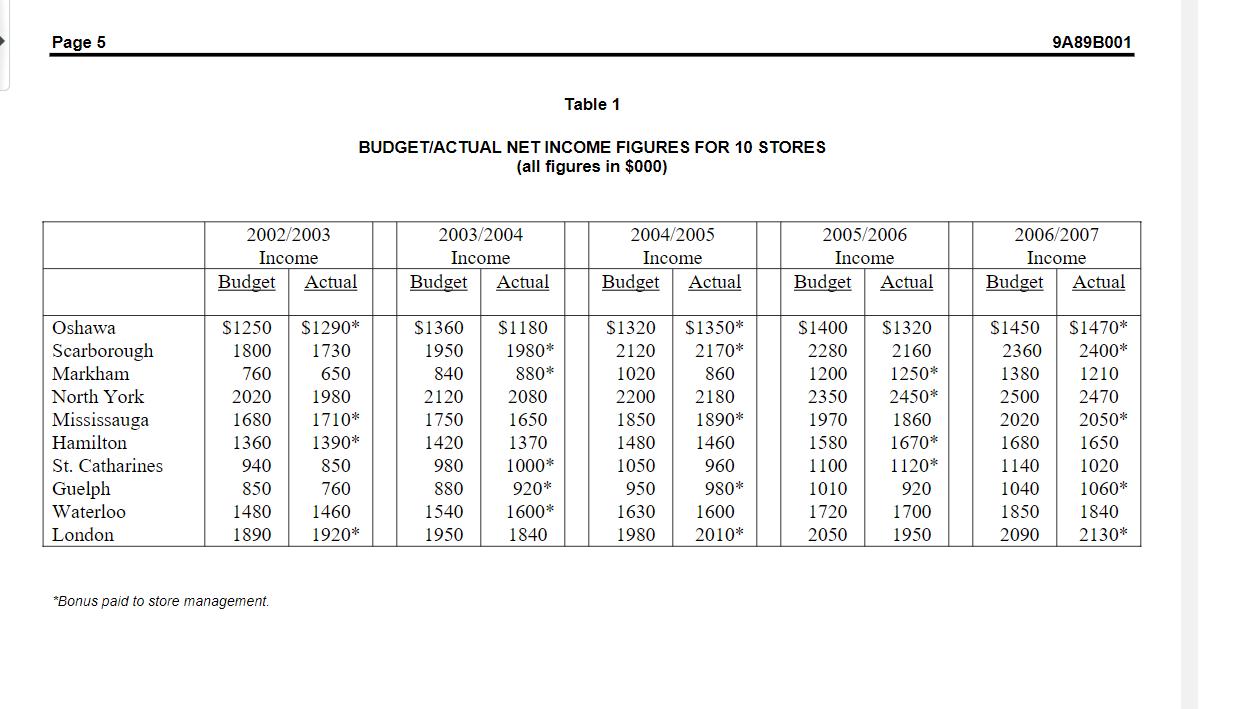

Assignment Questions: 1. What are the main issues facing John Smith? 2. What are the alternatives available for accounting, inventory, and advertising? How could these be used to manipulate income? 3. Should Acme management be concerned? Why? Why not? 4. What action should John Smith take based on the data currently available to him? 5. Any recommendations? ACME HARDWARE Alister K. Mason, Partner, Deloitte Haskins and Sells, Toronto, and Professor Claude Lanfranconi prepared this case solely to provide material for class discussion. The authors do not intend to illustrate either effective or ineffective handling of a managerial situation. The authors may have disguised certain names and other identifying information to protect confidentiality. written Ivey Management Services prohibits any form of reproduction, storage or transmittal without permission. This material is not covered under authorization from CanCopy or any reproduction rights organization. To order copies or request permission to reproduce materials, contact Ivey Publishing, Ivey Management Services, c/o Richard Ivey School of Business, The University of Western Ontario, London, Ontario, Canada, N6A 3K7; phone (519) 661-3208; fax (519) 661-3882; e-mail cases@ivey.uwo.ca. Copyright 2009, Ivey Management Services Version: (A) 2009-01-16 INTRODUCTION John Smith, C.A., was recently assigned the responsibility for the audit of Acme Hardware, a new client. He was wondering what action, if any, he should take about the way certain ores of Acme Hardware were accounting for inve and advertising costs. As a result of his pre-audit review of the previous auditor's files, he had identified a situation where there was a probability that certain store managers, motivated by the company's management and control system, were taking advantage of discretionary accounting alternatives available to them. Any complete investigation would be disruptive and expensive and had to be considered in light of the fact that the impact of their actions on the financial statements might be immaterial. company's THE COMPANY Acme Hardware was a rapidly expanding chain of hardware stores which operated in southern Ontario. All stores were company-owned; there were no franchises. By the beginning of the 2007/08 fiscal year, Acme had 14 stores, four of which had been opened up in the previous five years. Total sales in 2006/07 were $307 million (up from $214 million in 2002/2003), resulting in net income - after corporate expenses and income taxes of $12 million ($6.50 million in 2002/2003). Total assets as at March 31, 2007 were $174 million. College taught by S. Lamarre and S. Uddin from 01/10/2022 Authorized for use only in the course Capstone Course ACCT at Centennial Use outside these parameters is a copyright violation. Page 2 Acme's success was attributed to several factors, but the most important was usually considered to be the generous bonuses ($50,000), which were payable to the store manager when the budgeted net income for the year was met. Budgets were set by head office, after negotiations with store management. Net income was computed in accordance with accounting policies laid down by head office, and in the event of disagreement, Acme's auditors, who also reviewed each store's records, were to act as arbitrators. The predecessor audit firm had not been required to arbitrate any disagreements about the income computations in the preceding five-year period. PREPARATION FOR THE AUDIT Acme had recently engaged a new firm of auditors, Cooperhouse and Sells, and John Smith was the partner assigned to the engagement. In planning the work to be performed for the first year the year ended March 31, 2008 he reviewed the predecessor audit firm's working paper files. John found that the above-mentioned bonus arrangement had been identified by that firm as a potential "audit risk" with regard to the pressure on store managers to achieve budgets. John reviewed the budget and actual net income figures for the previous five years, to see how frequently the budgets had been met, and hence the bonuses paid. He noted that, for 10 stores he examined, because they had been in operation for some time, and therefore had an established pattern of operations, bonuses had been paid on 23 occasions (out of a maximum of 50). He also noted that, when a budget was met, the tendency seemed to be for it to be met by a narrow margin, but, when missed, by a much wider margin. ANALYSIS OF INCENTIVE SYSTEM To examine this issue more closely, John prepared a table setting out the budget and actual net income figures for the 10 stores over the five-year period (see Table 1). He separated the 10 stores into two groups: 1. Three stores (North York, Hamilton, and Waterloo) in which: (a) budgets were met four times out of a possible 15 (27 per cent); (b) the margins by which the budgets were met were $100,000, $30,000, $90,000 and $60,000 (average $70,000); and, (c) on the 11 occasions when the budgets were not met, the margins ranged from $50,000 down to $10,000 (average $28,000). 9A89B001 2. The other seven stores, for which: (a) budgets were met 19 times out of a possible 35 (54 per cent); (b) the margins by which the budgets were met ranged from $20,000 to $50,000 (average $33,000); and, (c) on the 16 occasions when the budgets were not met, the margins ranged from $70,000 to $180,000 (average $112,000). John concluded that there was a strong probability that the managers of seven stores were manipulating net income computations. Based on his experience, John thought that the most likely way of doing so would be by advancing or deferring - from one period to the next the recognition of income and/or expenses. For example: 1. By deferring the recognition of income or advancing the recognition of expenses, it would be easier to meet the budget in the next period. Managers would be tempted to do this when it was apparent say by the 10th or the 11th month of the fiscal year that (a) the current year's budget could not be met, or (b) the budget had already been met. 2. By advancing the recognition of income or deferring the recognition of expenses, it would be easier to meet the budget in the current period. This would be particularly tempting when, without action of this kind, the budget would probably be missed by a fairly narrow margin. John reviewed the monthly income statements for the individual stores, all of which followed a standard format (prescribed by head office), based on the income and expense accounts in the general ledger. He concluded that the two most likely areas for manipulation were: 1. Inventories These were valued at the lower of cost (determined on a FIFO first in first out basis) and net realizable value. The write-down to net realizable value was largely a matter of judgment, particularly in respect of seasonal merchandise, e.g., garden supplies, and products for which expected new models might make the present ones obsolete, e.g., power mowers. 2. Advertising Expenses Company policy required the costs of local advertising to be expensed in the period the campaign was run. However, store managers had discretion when a campaign should be run, and it would be quite possible to advance a campaign scheduled for the first week of April to the last week of March. (Experience had Page 4 shown that some advertising campaigns result in increased sales over the next few weeks, rather than only in the period in which the advertisements are run.) CONCLUSION John was very familiar with these types of incentive schemes because of their use by many of his other clients. He was also aware that senior management recognized that any management control system had flaws. However, these systems motivated their operating managers to maintain a focus on net income and, in the process, to maximize revenues and minimize costs. John also recognized that, unless several stores manipulated their results in the same direction in any year, the impact on the corporate financial statements would probably not be material. He now had to decide what, if any, action was necessary. 9A89B001 Page 5 Oshawa Scarborough Markham North York Mississauga Hamilton St. Catharines Guelph Waterloo London 2002/2003 Income Budget Actual $1250 $1290* 1800 1730 760 650 2020 1980 1680 1710* 1360 1390* 940 850 850 760 1480 1460 1890 1920* *Bonus paid to store management. BUDGET/ACTUAL NET INCOME FIGURES FOR 10 STORES (all figures in $000) 2003/2004 Income Budget Actual $1360 $1180 1950 840 1980* 880* 2120 1750 1420 980 880 1540 1950 Table 1 2080 1650 1370 1000* 920* 1600* 1840 2004/2005 Income Budget Actual $1320 $1350* 2120 2170* 1020 860 2200 2180 1850 1890* 1480 1460 1050 960 950 980* 1630 1980 1600 2010* 2005/2006 Income Budget Actual $1400 $1320 2280 2160 1200 1250* 2350 2450* 1970 1860 1580 1670* 1100 1120* 1010 920 1720 1700 2050 1950 9A89B001 2006/2007 Income Budget Actual $1450 $1470* 2360 2400* 1380 1210 2500 2470 2020 2050* 1680 1650 1140 1020 1040 1060* 1850 1840 2090 2130*

Step by Step Solution

★★★★★

3.41 Rating (151 Votes )

There are 3 Steps involved in it

Step: 1

The main issues facing John Smith include Low sales and declining revenue Overstocked inventory which ties up cash flow and incurs storage costs Limit...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Information System

Authors: James A. Hall

7th Edition

978-1439078570, 1439078572