Question

Assume that annual interest rate volatility is 25% and current Treasury par bond yields for various maturities are as follows: Maturity Par Rate 1 Year

Assume that annual interest rate volatility is 25% and current Treasury par bond yields for various maturities are as follows:

Maturity Par Rate

1 Year 1.28%

2 Years 1.87%

3 Years 2.04%

4 Years 2.07%

Construct a binomial interest rate tree, showing (1-year forward) rates at Years 0, 1, 2 and 3, that is consistent with the spot rates implied by the above par rates and the assumed interest rate volatility. Demonstrate that your tree correctly values a 6% annual coupon, $100 par value option-free bond with exactly 4 years to maturity.

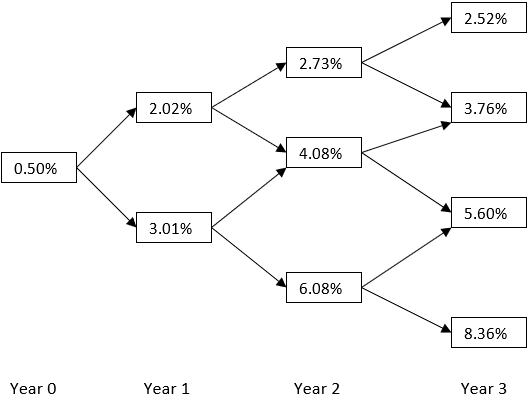

The interest rate tree diagramed below pertains to the next four questions. You may assume that all of the bonds being valued in these questions are free of default risk.

The tree assumes 20% annual interest rate volatility and is constructed from the following Treasury spot rates:

Year 1: 0.50%

Year 2: 1.50%

Year 3: 2.40%

Year 4: 3.00%

2.52% 2.73% 2.02% 3.76% 4.08% 0.50% 5.60% 3.01% 6.08% 8.36% Year 0 Year 1 Year 2 Year 3 2.52% 2.73% 2.02% 3.76% 4.08% 0.50% 5.60% 3.01% 6.08% 8.36% Year 0 Year 1 Year 2 Year 3Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investing For Women Smart Strategies To Start Investing Now With Confidence Low Risk And Minimal Effort

Authors: Mike Hartley ,Hannah Rosenstein

1st Edition

979-8393237202