Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Assume that expected factor returns are those given below: Expected Annualized Return 0.43% 9.72% 1.32% 4.44% rf rm -rf SMB HML Consider an asset,

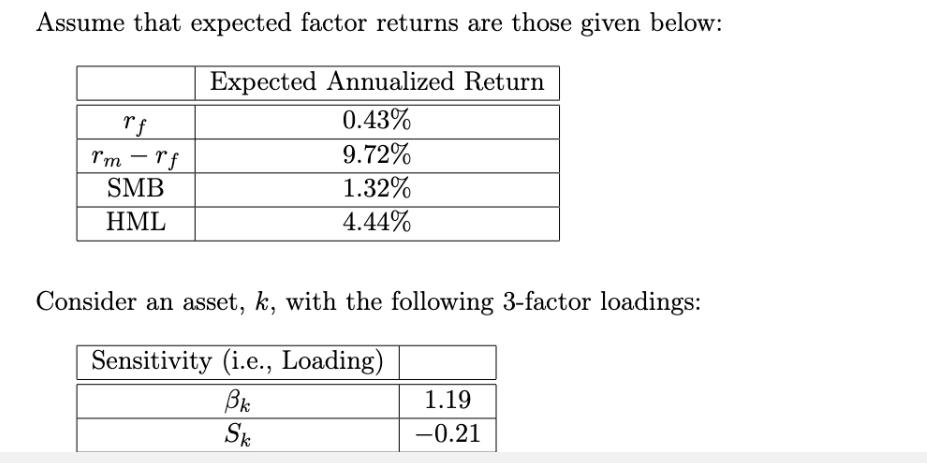

Assume that expected factor returns are those given below: Expected Annualized Return 0.43% 9.72% 1.32% 4.44% rf rm -rf SMB HML Consider an asset, k, with the following 3-factor loadings: Sensitivity (i.e., Loading) Bk Sk 1.19 -0.21 Hk -0.15 (i) Calculated the expected returns according to the Fama-French 3-factor model (1 point) (ii) Do you have enough information to calculate asset k's expected return with the CAPM? If so, calculate it, and show your work. If not, explain why not.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Basic Statistics

Authors: Charles Henry Brase, Corrinne Pellillo Brase

6th Edition

978-1133525097, 1133525091, 1111827028, 978-1133110316, 1133110312, 978-1111827021