Answered step by step

Verified Expert Solution

Question

1 Approved Answer

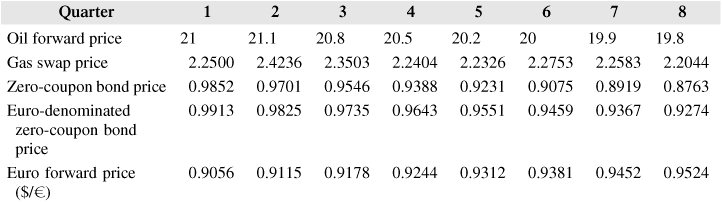

Assume that the current exchange rate is $0.90/ using the following table of information. Suppose that oil forward prices for 1 year, 2 years, and

Assume that the current exchange rate is $0.90/ using the following table of information.

- Suppose that oil forward prices for 1 year, 2 years, and 3 years are $20, $21, and $22. The 1-year effective annual interest rate is 6.0%, the 2-year interest is 6.5% and 3-year interest is 7%, what is the 3-year SWAP price?

- Supposing the effective quarterly interest rate is 1.5%, what are the per-barrel swap prices for 4-quarter and 8-quarter oil swaps? (Use oil forward prices in table) What is the total cost of prepaid 4- and 8-quarter swaps?

- Using the information about zero-coupon bond prices and oil forward prices in table, construct the set of swap prices for oil for 1 through 8 quarters.

- Using the information in table, what is the swap price of a 4-quarter oil swap with the first settlement occurring in the third quarter?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Project Financing Financial Instruments And Risk Management

Authors: Frank J Fabozzi, Carmel De Nahlik

1st Edition

9811231494, 9789811231490