Answered step by step

Verified Expert Solution

Question

1 Approved Answer

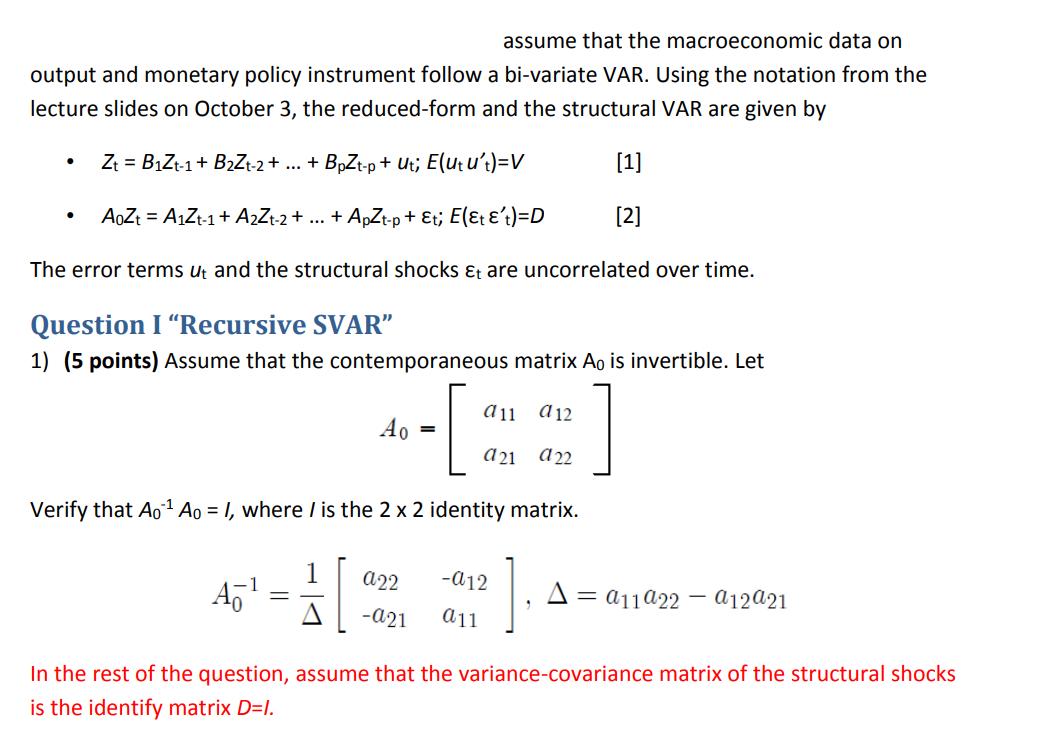

assume that the macroeconomic data on output and monetary policy instrument follow a bi-variate VAR. Using the notation from the lecture slides on October

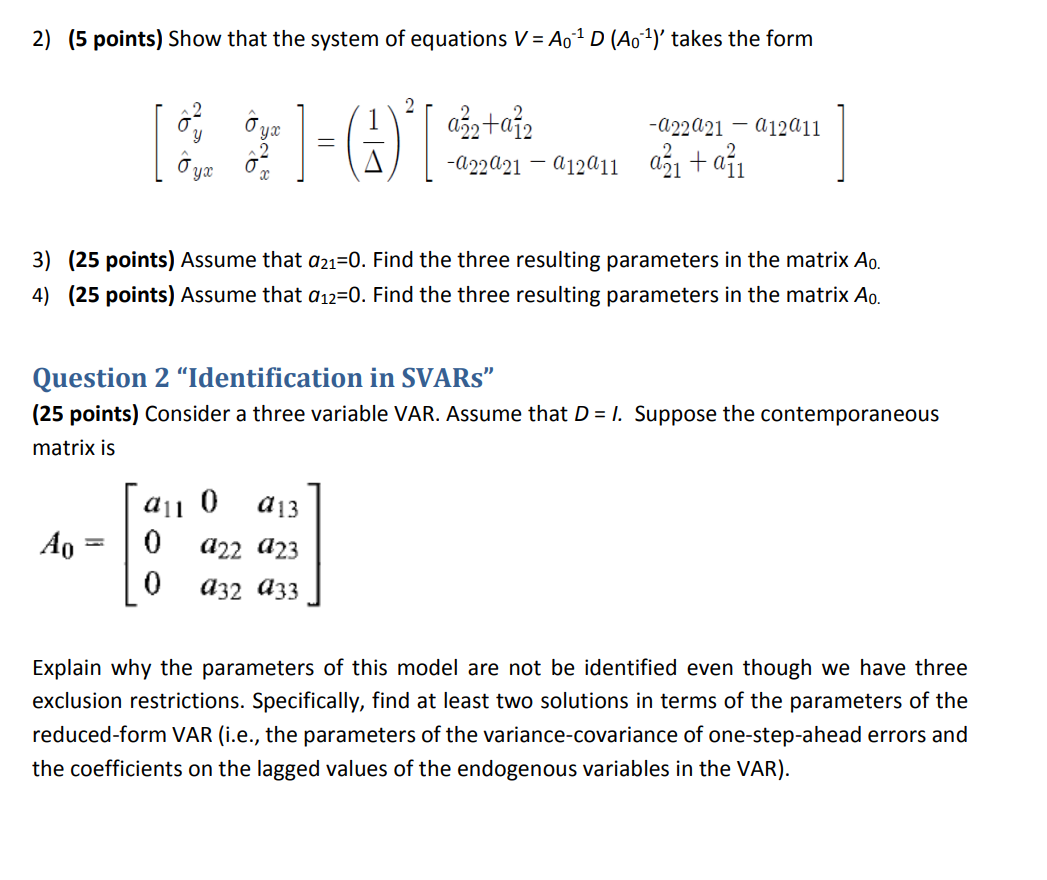

assume that the macroeconomic data on output and monetary policy instrument follow a bi-variate VAR. Using the notation from the lecture slides on October 3, the reduced-form and the structural VAR are given by Zt = B1Zt-1+ B2Zt-2 + ... + BpZt-p+ Ut; E(utu't)=V [1] AoZt=A1Zt-1 + A2Zt-2 + ... + ApZt-p + t; E(t 't) =D [2] The error terms ut and the structural shocks t are uncorrelated over time. Question I "Recursive SVAR" 1) (5 points) Assume that the contemporaneous matrix Ao is invertible. Let Ao = [ a11 a12 021 922 Verify that Ao A0 = 1, where / is the 2 x 2 identity matrix. A - a22 -012 -021 a11 A = a11a22a12a21 In the rest of the question, assume that the variance-covariance matrix of the structural shocks is the identify matrix D=I. 2) (5 points) Show that the system of equations V = A0 D (A0)' takes the form yx = 2 [ ] - (A) [ yx a22+a12 -a22a21 a12a11 -a22a21a12a11 a+a 3) (25 points) Assume that 021-0. Find the three resulting parameters in the matrix Ao. 4) (25 points) Assume that a12=0. Find the three resulting parameters in the matrix Ao. Question 2 "Identification in SVARS" (25 points) Consider a three variable VAR. Assume that D = 1. Suppose the contemporaneous matrix is Ao = a11 0 a13 0 422 423 a32 033 Explain why the parameters of this model are not be identified even though we have three exclusion restrictions. Specifically, find at least two solutions in terms of the parameters of the reduced-form VAR (i.e., the parameters of the variance-covariance of one-step-ahead errors and the coefficients on the lagged values of the endogenous variables in the VAR).

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Econometric Analysis

Authors: William H. Greene

5th Edition

130661899, 978-0130661890