Answered step by step

Verified Expert Solution

Question

1 Approved Answer

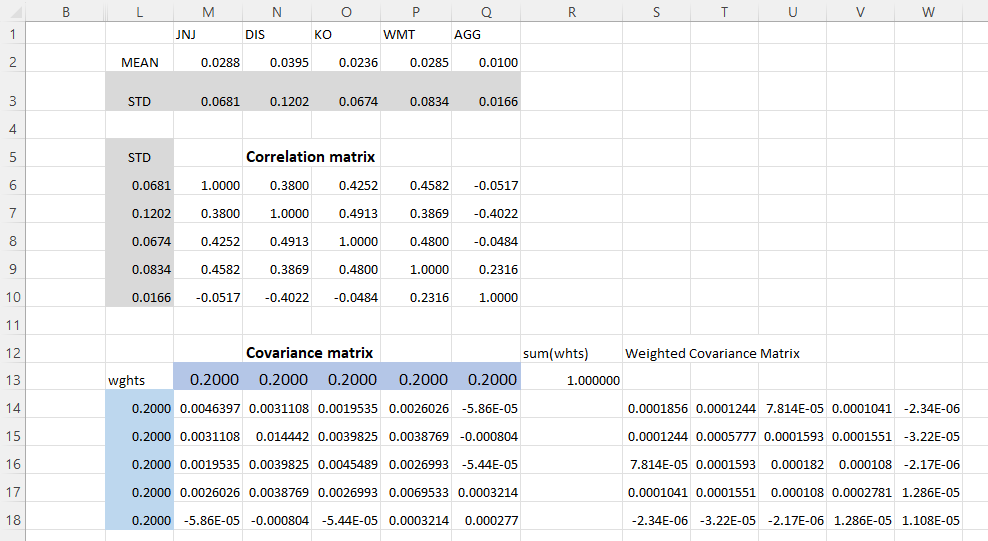

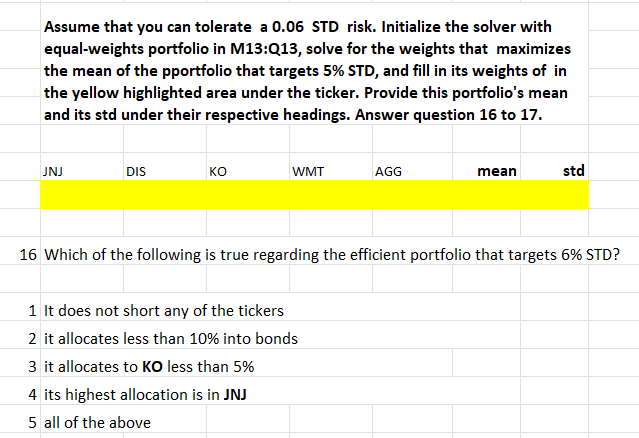

Assume that you can tolerate a 0.06 STD risk. Initialize the solver with equal-weights portfolio in M13:Q13, solve for the weights that maximizes the mean

Assume that you can tolerate a 0.06 STD risk. Initialize the solver with equal-weights portfolio in M13:Q13, solve for the weights that maximizes the mean of the pportfolio that targets 5\% STD, and fill in its weights of in the yellow highlighted area under the ticker. Provide this portfolio's mean and its std under their respective headings. Answer question 16 to 17. \begin{tabular}{|l|l|l|l|l|l|} \hline JNJ KO & WIS & WMT & AGG & mean \end{tabular} 16 Which of the following is true regarding the efficient portfolio that targets 6% STD? 1 It does not short any of the tickers 2 it allocates less than 10% into bonds 3 it allocates to KO less than 5% 4 its highest allocation is in JNJ 5 all of the above

Assume that you can tolerate a 0.06 STD risk. Initialize the solver with equal-weights portfolio in M13:Q13, solve for the weights that maximizes the mean of the pportfolio that targets 5\% STD, and fill in its weights of in the yellow highlighted area under the ticker. Provide this portfolio's mean and its std under their respective headings. Answer question 16 to 17. \begin{tabular}{|l|l|l|l|l|l|} \hline JNJ KO & WIS & WMT & AGG & mean \end{tabular} 16 Which of the following is true regarding the efficient portfolio that targets 6% STD? 1 It does not short any of the tickers 2 it allocates less than 10% into bonds 3 it allocates to KO less than 5% 4 its highest allocation is in JNJ 5 all of the above Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding financial statements

Authors: Lyn M. Fraser, Aileen Ormiston

9th Edition

136086241, 978-0136086246