Answered step by step

Verified Expert Solution

Question

1 Approved Answer

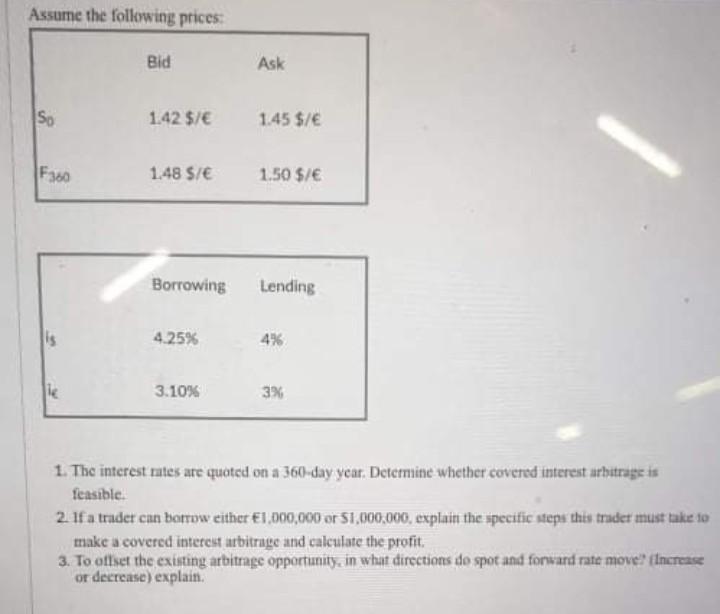

Assume the following prices: Bid Ask So 1.42 $/ 1.45 $/ F360 1.48 S/ 1.50 $/ Borrowing Lending lis 4.25% 4% 3.10% 3% 1. The

Assume the following prices: Bid Ask So 1.42 $/ 1.45 $/ F360 1.48 S/ 1.50 $/ Borrowing Lending lis 4.25% 4% 3.10% 3% 1. The interest rates are quoted on a 360-day year. Determine whether covered interest arbitrage is feasible. 2. If a trader can borrow either 1,000,000 or 51,000,000, explain the specific steps this trader must take 10 make a covered interest arbitrage and calculate the profit. 3. To offset the existing arbitrage opportunity. In what directions de spot and forward rate move? Increase or decrease) explain. Assume the following prices: Bid Ask So 1.42 $/ 1.45 $/ F360 1.48 S/ 1.50 $/ Borrowing Lending lis 4.25% 4% 3.10% 3% 1. The interest rates are quoted on a 360-day year. Determine whether covered interest arbitrage is feasible. 2. If a trader can borrow either 1,000,000 or 51,000,000, explain the specific steps this trader must take 10 make a covered interest arbitrage and calculate the profit. 3. To offset the existing arbitrage opportunity. In what directions de spot and forward rate move? Increase or decrease) explain

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started