Answered step by step

Verified Expert Solution

Question

1 Approved Answer

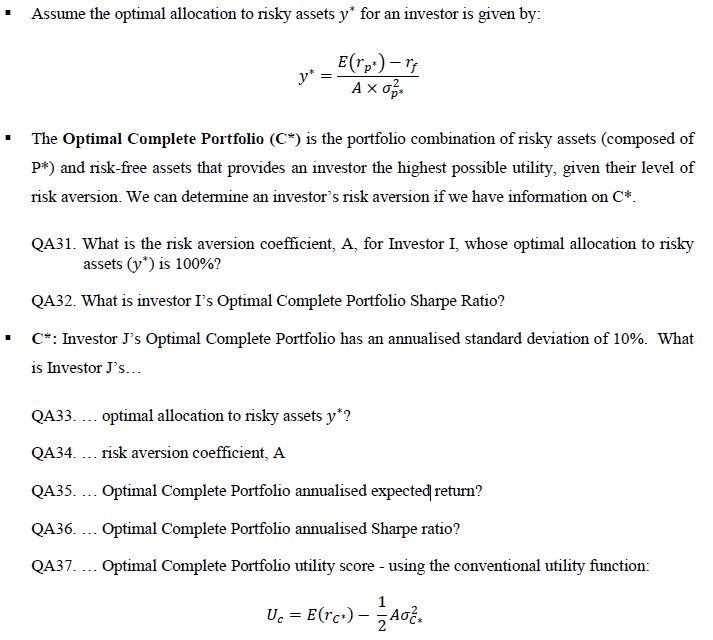

Assume the optimal allocation to risky assets y* for an investor is given by: E(rp) - rf Axo y: The Optimal Complete Portfolio (C*)

Assume the optimal allocation to risky assets y* for an investor is given by: E(rp) - rf Axo y": The Optimal Complete Portfolio (C*) is the portfolio combination of risky assets (composed of P*) and risk-free assets that provides an investor the highest possible utility, given their level of risk aversion. We can determine an investor's risk aversion if we have information on C*. QA31. What is the risk aversion coefficient, A, for Investor I, whose optimal allocation to risky assets (y) is 100%? QA32. What is investor I's Optimal Complete Portfolio Sharpe Ratio? C*: Investor J's Optimal Complete Portfolio has an annualised standard deviation of 10%. What is Investor J's... QA33. ... optimal allocation to risky assets y*? QA34.... risk aversion coefficient, A QA35. ... Optimal Complete Portfolio annualised expected return? QA36.... Optimal Complete Portfolio annualised Sharpe ratio? QA37.... Optimal Complete Portfolio utility score - using the conventional utility function: 1 Uc = E(rc+) - Ao2.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Statistics For Management And Economics Abbreviated

Authors: Gerald Keller

10th Edition

978-1-305-0821, 1285869648, 1-305-08219-2, 978-1285869643