Answered step by step

Verified Expert Solution

Question

1 Approved Answer

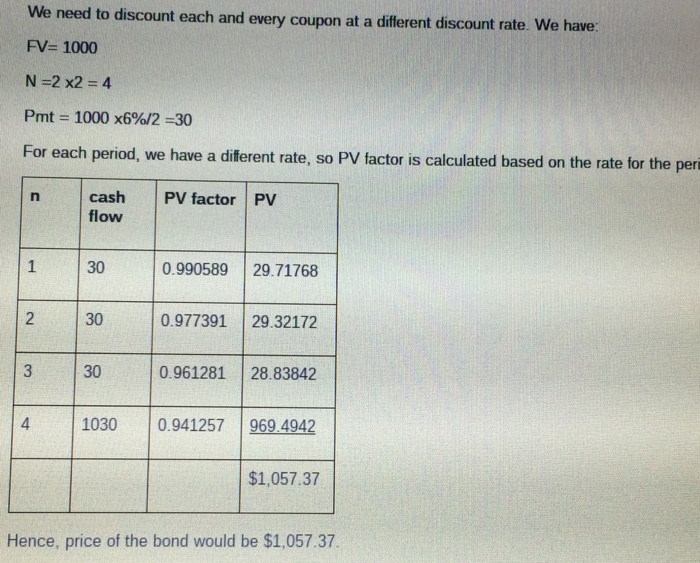

Assuming the market is arbitrage-free, if a six-month pure discount bond yields 1.9%, a one year-pure discount bond yields 2.3%, an eighteen-month bond yields 3.05%,

Assuming the market is arbitrage-free, if a six-month pure discount bond yields 1.9%, a one year-pure discount bond yields 2.3%, an eighteen-month bond yields 3.05%, what should be the price of a two-year discount bond yields 3.05%, what should be the price is a two-year $1,000 6% par-value bond with semiannual coupons?

Answer: $1,057.82

I asked this question before and recieved the answer below. However, my question now is how was the PV factor calculated. I attempted to calculate it and I am off be a few decimals which may not be a big deal but I am just unsure if I am actually doing the correct calculation.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Health Care Financial Management

Authors: Steven Berger

4th Edition

1118801687, 978-1118801680