Question

Asume the convexity is scaled by the bond price, i.e. A par bond price is B=100$. Interest rate increase by 1% makes the price B(+1%)

Asume the convexity is scaled by the bond price, i.e.

A par bond price is B=100$.

Interest rate increase by 1% makes the price B(+1%) = 97$.

Interest rate decrease by 1% makes the price B(-1%) = 101$.

What is the convexity of a bond?

Use the decimals for the rate, 0.01 for 1%.

What is the convexity of a bond? Use the decimals for the rate, 0.01 for 1%.

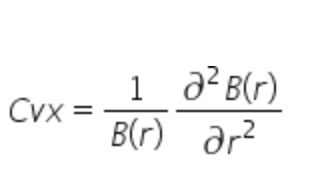

Cvx= 1 dB a2B(r) B(r) ar

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Freedmans Handbook A Practical Guide To Wealth

Authors: Wilfred Brown, Adrian Tullock

1st Edition

1478748400, 978-1478748403